A couple of months ago I spent eight days crossing America — Indianapolis to Cincinnati, Boston, New York, and finally Omaha for the Berkshire Hathaway annual meeting — visiting businesses, investors, ballparks, bookstores and art galleries.

On the surface, the itinerary made little sense. Fire safety equipment, diesel engines, uniform rental, furniture stores, hedge funds, modern art and baseball do not naturally belong together.

But that's part of why I keep doing these trips. The best ideas rarely stay confined to one discipline. A manufacturer can teach you about culture. An artist can teach you originality. A ballplayer can teach you patience. A retailer can teach you customer obsession. A great investor can teach you temperament.

One question ran underneath almost every conversation:

What allows certain people, businesses and organisations to compound for decades?

Indianapolis — fire safety and taking the long view

The first few meetings could hardly have looked more different. MSA Safety first came onto my radar the way some of the best ideas in investing do — not through a screen, but through another investor’s work. Sequoia flagged the business in its 2025 letter. We caught up with the company and management at the world’s largest firefighting conference, held in Indianapolis.

MSA built its position protecting firefighters and industrial workers through a genuine customer obsession — designing alongside the people who actually use the equipment, not just for them. That trust has compounded over decades into the number one or two market share in category after category. Now the company is using technology to widen that moat further, connecting equipment to central systems that give responders better information in real time and help save more lives.

Spending time with CEO Steve Blanco was genuinely comforting. While the analyst community obsesses over next quarter's earnings, Steve is investing for the decade ahead — new product platforms. It's a reminder that some of the best management teams are quietly ignoring the very audience that's watching them most closely. Meeting not just Steve but several divisional managers, the same pride and passion for the mission showed up at every level — a good sign for a business whose edge depends on genuinely caring about the people who use its equipment, not just selling to them.

Perimeter Solutions, the fire retardant business, has its own version of a hard-to-crack niche — regulatory and certification hurdles keep the field narrow — backed by the TransDigm founder and Will Thorndike running a serial-acquirer playbook over it.

Cincinnati / Columbus — Cintas, and a century-old diesel company's town

Cintas is a 750-bagger, and it's tempting to look for a hidden secret behind a number like that — a breakthrough product, a stroke of genius.

Sitting with CEO Todd Schneider and COO Jim Rozarkis, the real answer was far less exciting: culture, execution, measurement, internal competition, and a customer obsession that shows up in the small things — route reliability, uniform improvements and responsiveness — repeated for decades. Both men started at the bottom of the business and worked their way through it, and it shows — the culture emanates out of two people who lived every layer of it themselves.

I asked what people notice most when they join. The answer — "you people are crazy." Cintas is intensely competitive, everything is measured, and the intensity shakes plenty of people out early. It's part of why they like hiring straight out of college and promoting from within — training people into the culture before they've been shaped by anywhere else. For the ones who like being measured and like competing, it becomes the kind of place they stay for good.

What struck me most, though, was how much runway is still ahead of it. The market remains underpenetrated, with plenty of whitespace and a genuine value-add proposition for customers who haven’t yet switched. It’s also highly fragmented — and growth comes as much through courtship as through competition, with M&A built on relationships developed over decades.

Cummins offered a different version of the same idea. 46 years of 15.5% annual compounding through every kind of adversity — oil shocks, emissions regulation, entire technology cycles — but the legacy isn't only in the numbers.

J. Irwin Miller led the company for some 40 years and understood that businesses could shape communities, not just serve them. He commissioned some of the twentieth century’s greatest architects to remake Columbus, Indiana — a town of just over 50,000 people that the American Institute of Architects ranks the sixth most architecturally significant city in America, behind only Chicago, New York, Boston, San Francisco and Washington, D.C.

An entire town built on the idea that buildings shape people. The evidence of a truly great company sits not just in its financial statements, but in the streets around it.

Boston — museums, Fenway, and the limits of theatre

RH Design, the luxury furniture retailer, was its own kind of lesson, and one better learned in person than from a spreadsheet. Walking through their galleries — first at the DeHaan Estate in Indianapolis, then again across four floors of the old Museum of Natural History in Boston — it's impossible not to be impressed: manicured, château-like grounds, restaurant service. This is closer to theatre than retail. But that differentiation comes with a burden competitors don't carry — fit-out and upkeep at that standard, in every gallery, indefinitely. And once you look past the staging, the heritage, quality and differentiation feel a long way from an Hermès or even a Louis Vuitton — brands that pair the theatre with generations of craft underneath it. Beautiful businesses still have to earn their keep.

The Museum of Fine Arts, the Isabella Stewart Gardner, and later MoMA and the Joslyn, all taught some version of the same thing about originality — none of the artists whose work hangs there succeeded by copying consensus, and the crowd rarely recognises that kind of originality on time.

In the last few years I've gone down a rabbit hole reading about some of the greatest artists and art dealers, trying to understand where creativity actually comes from — and why it so often takes the market a long time to recognise genius. Van Gogh, de Kooning, Robert Henri, Pollock, Edward Hopper, among others: standing in front of their paintings with that history front of mind adds an entirely different layer to experiencing the work. Hopper put it best on originality itself: "Originality is neither a matter of inventiveness nor method in particular a fashionable method. It is far deeper than that, and it is the essence of personality."

Great businesses and great investors seem to share the same streak of independence. They're willing to challenge conventional wisdom, and they bring something close to a fanatical approach to their craft. Perhaps Hopper's real gift was seeing the simplicity sitting inside the complexity — stripping a scene down until only the essential thing remained. The best investors do something similar with a business. The method looks different. The temperament underneath it doesn't.

At Fenway Park, the 114-year-old home of the Boston Red Sox and the oldest active ballpark in Major League Baseball, the story was Ted Williams — the longest home run ever hit there, 502 feet, in 1946, a record that still stands. Buffett took the lessons of one of America's greatest sportsmen and applied them to investing: he keeps Williams's photo on his office wall, and wrote in 1997 that great investing needs exactly this kind of discipline — waiting for the fat pitch, swinging only at the best of it. Activity feels productive. Selectivity is the actual edge.

Boston / New York — patient capital, and the ideas business

The investors mostly circled back to one theme: temperament and time are the edge, far more often than analysis.

At Abrams Capital, Raja Bobbili described their advantage as behavioural rather than purely analytical — patient capital lets you support management through hard periods and go on the offensive when others are retreating — adding conviction while the market panics, and staying focused on business value instead of the daily price. It's a concentrated approach run by a four-person investment team. Their involvement in the new ContextLogic, built around the old US Salt business, is a structure worth watching — framed on the model of the Swedish compounders, giving management genuine long-term exposure rather than a typical private-equity exit path, and designed to attract the kind of management teams who want long-term partners, not short-term owners.

Seth Klarman made a related point at Baupost: as the market grows more short-term, it may be growing more inefficient for anyone still willing to hold a longer view. A nice paradox — the more impatient the world gets, the more valuable patience becomes.

At Oaktree, Howard Marks talked about building a firm around principles rather than personalities — intelligence, independent thinking, team culture — the same ingredients that let a business, not just a fund, survive beyond its founders. He was emphatic that culture comes first: no matter how successful someone is, if they don't live up to the standards integral to the business, they don't belong at Oaktree.

New York offered its own lesson, at the ballpark rather than the boardroom. The Knicks playoff game at Madison Square Garden was pure electricity — a city that takes its basketball seriously. A night later at Citi Field, the contrast was stark: a Nationals grand slam helped the Mets to their heaviest defeat of the season, and the stands were half empty. Same city, same week, two very different atmospheres. Winning teams fill stadiums.

At Sequoia Fund, Arman and Trevor described their work simply as the ideas business. Research into one company leads to its suppliers, its competitors, its customers, and often the more interesting idea sitting one step away from the one you started with. A company that isn't interesting today might be interesting tomorrow — there's a real cost to closing your mind too early. They were candid about the market's winner bias too: a small number of positions usually drive the bulk of long-run returns. Finding them is hard. Holding them, they said, is harder — this is ultimately a behavioural business.

Michael Baron made the same point from a different angle. Baron Capital's seven-to-eight year average holding period isn't an accident; it's a structure built to give a good business enough time to surprise you. He's understood the idea since he was a kid at the dinner table with his father, Ron: it's the fundamentals, not the macro, that matter — and you still need balance across a portfolio, because being all-in on one position is how you get burnt.

Munib Islam at Saraza Management framed it in the sharpest terms of the trip. He sorts every business into three buckets: great companies that stay great, great companies quietly slipping to good, and good companies becoming great.

It's the middle category that does the damage — a business can look wonderful in the rear-view mirror while its future is already eroding, which is why he treats quality as something that's never stationary, scoring it fresh rather than assuming it holds.

His favourite question for management says most of what needs saying: "What are you doing right now to make your moat wider?" — often revealing simply in how hard it is to answer.

And on the two traits that actually separate investors, he was blunt: temperament — most pod shops have none for volatility — and duration, the willingness to sit through real discomfort. "We don't have to be early," he said. "We just have to be there for the ride."

Omaha — the last lesson

Breakfast with Chris Begg of East Coast Asset Management was a highlight of Omaha. I’ve enjoyed his writing for almost two decades — he’s one of the most thoughtful investors around, and one of the few who genuinely embodies the multidisciplinary thinking Munger used to talk about. He’s now leveraging AI to sharpen his investment process, folding new tools into a mind that’s spent years pulling ideas from philosophy, architecture, and history as readily as from financial statements.

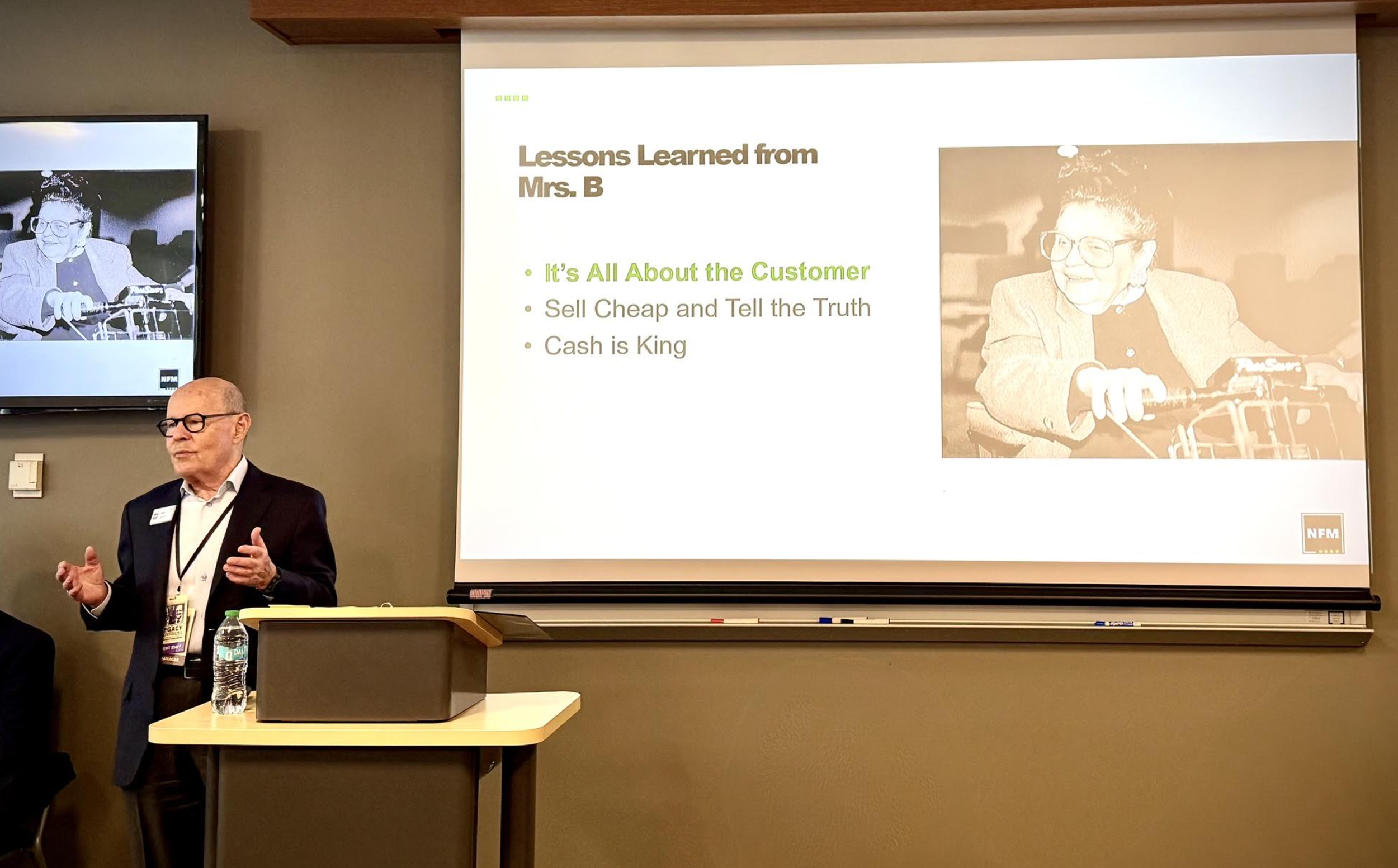

For seven years I've listened to Ron Blumkin and the team at Nebraska Furniture Mart trace the business back to the lessons of Mrs B: sell cheap, tell the truth, look after the customer. Nearly ninety years later, none of it has changed. "We are a learning machine," Ron told us. "I really mean that." Here's a family that built one of America's great retailers, sold it to Berkshire, and still keeps travelling to Harvard for leadership courses — 26 times and counting. Success never convinced them they had the answers. It convinced them to keep looking for better ones.

They remain just as obsessed with the customer end of the business — happy to be comparison shopped, because they believe they'll win, and unwilling to give away the low end of the market the way Sears once did. Sears forgot that lesson. Walmart didn't.

Eight days. Completely different industries, completely different people. And yet the same ideas kept resurfacing — in a diesel engine's hundred-year town, in a hedge fund's four-person investment team, in a 1946 home run that's never been beaten, in a family that still hasn't stopped learning after ninety years.

The advantage was rarely some complicated formula.

It was the willingness to keep learning, keep improving, and keep doing the right things for long enough.

* Visit the Blog Archive *

Learn more with us on Twitter: @mastersinvest

TERMS OF USE: DISCLAIMER