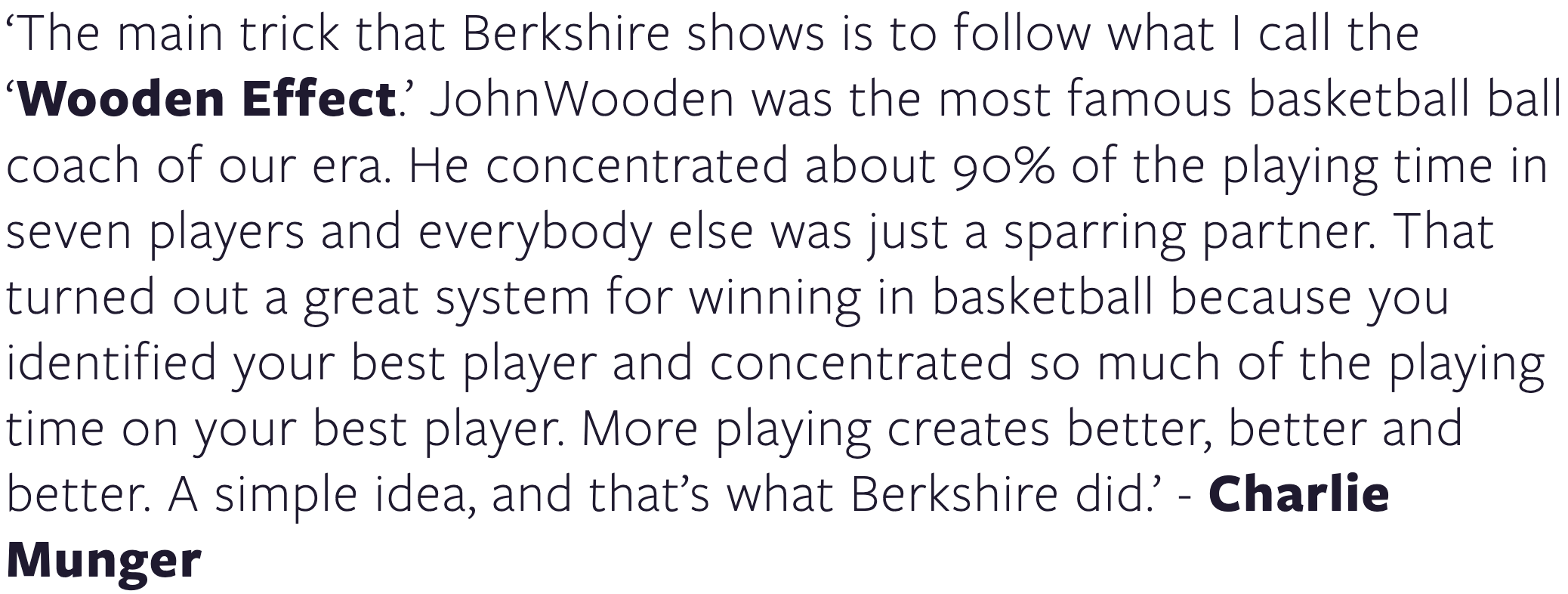

In his last interview, Charlie Munger recognized the foundation of Berkshire's triumph, attributing it to what he termed the 'Wooden Effect'—a concept inspired by John Wooden's method of allocating playing time to the team's most exceptional players.

Munger hailed John Wooden as the preeminent basketball coach of his era, boasting an impressive track record that included 10 NCAA championships in a remarkable 12-year span, seven consecutive titles, and an unparalleled 88-game winning streak.

What sets Wooden apart is not merely his extraordinary success but his unconventional approach to attaining it. Rather than relentlessly pursuing victory, he embraced a philosophy that transcended the fixation on winning. Wooden articulated, "I never talked about winning to our players. When you start fixating on winning, you lose sight of doing your job." This perspective imparts a profound lesson extending well beyond the basketball court: success is not the primary goal; instead, it's the natural outcome of pursuing a higher purpose. Wooden's unwavering commitment to the process, hard work, and dedication not only yielded an extraordinary basketball record but also offers profound insights applicable to businesses striving for success.

Wooden's leadership principles extended to empowerment and granting permission to fail, recognizing that 'over-coaching' can dampen intrinsic motivation and impede self-driven growth. He understood that encouraging autonomy and embracing failure as part of the journey are essential components of success, whether on the court or in the corporate world.

Wooden's success resulted from what Charlie Munger terms 'Lollapalooza' effects—greatness achieved not through a single grand strategy but through countless small deliveries of excellence. This dedication to continuous improvement aligns with the core tenets of many great businesses, emphasizing that the culmination of lots of little things creates a competitive edge that's almost impossible to compete with.

Wooden's emphasis on developing everyone within the organization created a team spirit from which emergent effects arose—an enchanting synergy that occurs when individuals willingly sacrifice personal interests for the collective good. Effective business leaders should aim to create an environment where each member's contribution is valued and vital to the organization's success, echoing Wooden's belief in unlocking the potential of every team member. Learning and continuous improvement were non-negotiable in Wooden's playbook—never settling for the status quo. His philosophy echoes the idea that success is a journey rather than a destination, demanding a perpetual drive to become a little better each day. Wooden's wisdom illuminates the path to building great businesses, reminding us that success isn't a finite goal but an ever-evolving expedition.

Over the years, my reading list has been filled with numerous books on great businesses, exceptional managers, and successful leaders. Yet, John Wooden's book, penned in his ninth decade of life, stands out as one of the most inspiring and deeply insightful works I've encountered. Delving into 'Wooden on Leadership' is akin to enrolling in a master class on the essential traits necessary for both personal success and the effective management of a thriving organization. At its core, whether discussing an elite sports team or a prosperous business enterprise, the common denominator is people.

The undeniable parallels between Wooden's wisdom and the principles of the great CEOs we've studied make it challenging to envision anyone applying the insights from this book not achieving success. I've ordered copies for my older sons entering their careers, ensuring they benefit from its invaluable wisdom.

Below are some favorite passages, offering a glimpse into the wealth of insights within.

Obliquity

‘I never talked about winning to our players. When you start thinking about winning, you stop thinking about doing your job.’

‘For most of my life I have believed that success is found in the running of the race. How you run the race, your planning, preparation, practice, and performance counts for everything. Winning or losing is a by-product, an after-effect, of that effort.’

‘I do not judge success based on championships; rather, I judge it on how close we came to realising our potential.’

‘Winning is a by-product. Focus on the product: effort.’

‘I never fixated on winning - didn’t even mention it.’

‘An organisation – a team – that’s always looking up at the scoreboard will find a worthy opponent stealing the ball right out from under you. You must keep your eye on the ball, not up on the scoreboard or somewhere out in the distant future. This task, however, is not always easy to do.’

‘The score will take care of itself when you take care of the effort that precedes the score.’

‘Let me be clear; Results matter. They matter a great deal. But if this is an organisation’s singular purpose, then the people who sign on are often often doing it for the wrong reasons.’

‘A person who values winning above anything will do anything to win. And such people are threats to their organisations.’

Success and The Controllables

‘There is a standard higher than merely winning the race: Effort is the ultimate measure of your success.’

‘I do not judge success based on championships; rather, I judge it on how close we came to realising our potential.’

‘Success - peace of mind which is the direct result of self-satisfaction in knowing you did the best of which you are capable - became the stated objective or destination for those I was teaching and coaching.’

‘I gradually disciplined myself and later the teams I taught, coached, and led, to focus on and worry about only those things we controlled, namely, getting as good as we could get, striving to reach the ultimate of our capabilities both mentally and physically. Whether that might, or did, result in outscoring our opponent - ‘winning the race’ - was something I didn't lose much sleep over.’

‘My final words were always about the same: ‘When it's over, I want your heads up. And there's only one way your heads can be up that's to give it your best out there, everything you have.’ This is all I ever asked of them because it was all they could ever give.’

‘To my way of thinking, when you give your total effort - everything you have - the score can never make you a loser. And when you do less, it can't somehow magically turn you into a winner.’

Source: UCLA

“For most of my life I have believed that success is found in the running of the race. How you run the race - your planning, preparation, practice, and performance counts for everything. Winning or losing is a by-product, an aftereffect, of that effort. For me, it's the quality of your effort that counts most and offers the greatest and most long-lasting satisfaction.

Cervantes had it right: "The journey is better than the inn." Most people don't understand what he means, but thanks to my father I do. The joy is in the journey of pushing yourself to the outward limits of your ability and teaching your organization to do the same.

I believe most great competitors share this feeling. They recognize that the ultimate reward is in the competitive process itself rather than some subsequent gain or glory brought about by winning. Thus, in all my years of coaching I rarely, if ever, even uttered the word win, talked about "beating" an opponent, or exhorted a team to be number one, including those picked by experts to win national championships.”

‘We are paid to deal with fate. Those who prevail look fate in the eye and say, ‘Welcome,’ and then move ahead without complaint, excuse, or whining. While we can't control fate, we are or should be able to control our response to it. In leadership, your response becomes crucially important, because ultimately it is the response of your organization.’

‘As a coach and leader I tried hard to avoid letting those things I couldn't control affect the things I could control. In more than nine decades I have yet to control fate. Neither have you, I'm sure.’

Value, Empower and Teach

‘When the best leader’s work is done the people say, ‘We did it ourselves.’’ Lao-tse

‘As a teacher, coach, and leader, my goal was always to help those under my leadership reach the ultimate level of their competency, both individually and as productive members of our team.’

‘From my earliest days I have viewed my primary job as one of educating others: I am a teacher. I believe effective leaders, are first and foremost, good teachers. We are in the education business.’

‘Knowledge is not enough. You must be able to effectively transfer what you know to those you manage - not just the nuts-and-bolts material, but your standards, values, ideals, beliefs, as well as your way of doing things.’

‘Many managers and coaches take for granted that people who work with them know how their efforts help the organisation. This is often not the case, especially for those in lesser roles. Go out of your way to make them feel included rather than excluded from the productivity you seek. Thank them for their efforts - if deserved - and explain why their work matters band how it contributes to the welfare of the group.’

‘‘Over-coaching’ can be more harmful than ‘under-coaching.’ Don’t give them too much and don’t take away their initiative.’

‘I didn’t want UCLA to crash because people weren’t doing their jobs because they felt their contributions didn’t count much.’

‘Acknowledge the unacknowledged. I was conscious about making those with less significant roles feel valued and appreciated. I singled out individuals who seldom saw the limelight - the player who made an assist on an important basket, a pivotal defensive play, or a free throw at a crucial moment in the game.’

‘All members of your organisation need to feel their jobs make a difference, that they are connected to the success of their team.’

‘The person who answers the telephone at your company plays a role in your success (or lack thereof). Do this person and the others who perform the tasks that make your organisation really ‘hum’ understand their connection and contribution? Do you let these individuals know, for example, how important that first contact with a potential customer or client is? Or do you let them operate in a vacuum, unconnected to everything around them? The telephone operator and all others who may perform less ‘important’ tasks will not feel important unless you, the leader, teach that them they are valued and explain how their contribution helps the company as a whole. Individuals who feel they don't matter will perform their jobs as if they don't count.’

‘I believe that personal greatness is measured against one’s own potential, not against that of someone else on the team or elsewhere.’

‘Some years, the teams I taught were blessed with significant talent. Other years, this was not the case. But in all years - with all levels of talent - my goal was the same, namely, to get the most out of what we had.’

Hard Work

‘There is no trick, no easy way to accomplish the difficult task, no substitute for old-fashioned work.’

‘For the Wooden family, hard work was as common as dirt - and dirt is common on a farm.’

Fun and Optimism

‘Work without joy is drudgery. Drudgery does not produce champions, nor does it produce great organisations.’

‘Coach Wooden dealt in the positive. He would not spend time on the negative - he was always focusing on moving forward with what we had to learn to make us better.’ Fred Slaughter

Hiring

‘Seek players who will make the best team rather than the best players. Astute leadership understands the chemistry of teams and organisations. Often the most talented individuals will not be a good for your group. Be alert to overall impact - chemistry.’

‘Bad habits are even tougher to break when it comes to character issues [ie good values]. I didn't kid myself into thinking that just because a player had great athletic talent, I could change his bad habits in these most important areas. I believe effective leadership is very cautious about bringing bad habits into the group. More often than not, before you can break their bad habits, they have taught those habits to others on your team.’

Kareem Abdul-Jabbar and John Wooden

‘Surround yourself with people strong enough to change your mind. I believe that you must have people around you willing to ask questions and express opinions, people who seek improvement for the organization rather than merely gaining favor with the boss. Look for these people when hiring and making promotion decisions.’

‘Throughout my career I had a policy of doing virtually no off-campus recruiting of student-athletes. If he wasn't eager to join us, then perhaps it was best he attended another school.’

‘Seek those with fire-in-the-belly enthusiasm for your organisation.’

‘I sought character in players rather than players who were characters.’

‘If you don’t care what kind of person you have on your team so long as they help the team win, I question whether you’ll attain consistent long-term success.’

‘Character is not taught easily to adults who arrive at your desk lacking it. Be cautious about taking on ‘reclamation projects’ regardless of the talent they may possess.’

Permission to Fail

‘The most effective leaders understand that failure is a necessary ingredient of success.’

‘A basketball team that won’t risk mistakes will not outscore opponents. The same is true for any organisation. Fouls, errors, and mistakes are part of the competitive process in sports, business and elsewhere. Don’t live in fear of making a mistake.’

‘Do not be afraid of mistakes, even of failure. Use good judgement based on all available information and then use initiative. The leader who has a fear of failure, who is afraid to act, seldom will face success.’

‘Even well-reasoned actions can fail. Mistakes and failed action are part of progress.. When you punish your people for making a mistake or falling short of a goal, you create an environment of extreme caution, even fearfulness. In sports it’s similar to playing ‘not to lose’ - a formula that often brings on defeat.’

‘Members of an organisation always fearful or penalty and punishment are at a great disadvantage when competing against a team filled with pride. This is so particularly over the long haul.’

Lollapalooza

‘There was no single big thing that made our UCLA basketball teams effective, not the press or the fast break, not size, not condition- no single big thing. Instead, it was hundreds of small things done the right way, and done consistently.’

‘High performance and production are achieved only through the identification and perfection of small but relevant details - little things done well. Those under your leadership must be taught that little things make the big things happen. In fact, they must first learn there are no big things, only a logical accumulation of little things done at a very high standard of performance.’

‘I derived great satisfaction from identifying and perfecting those ‘trivial’ and often troublesome details, because I knew, without doubt, that each one brought UCLA a bit closer to our goal; competitive greatness.’

‘Little things done well, make big things happen for you and your organisation.’

‘When you derive pleasure and pride in perfecting seemingly "minor" details and teach those you lead to do the same--big things eventually start falling into place. This is what separates achievers from the also-rans, the great from the good, the doers from the dreamers.’

Emotions

‘Although you may not be able to control what fate brings your way, you can control how you react and respond to it. At least you should be able to.’

‘Emotionalism destroys consistency. A leader who is ruled by emotions, whose temperament is mercurial, produces a team whose trademark is the roller coaster - ups and downs in performance; unpredictability and undependability in effort and concentration; one day good, the next day bad.

This is a pattern I sought to avoid at all costs. I would not accept inconsistency - the pitfalls of repeated highs and lows. I wanted the individuals on our team to play the same way, game to game, that is, with the greatest intensity while executing at the highest performance level of which they were capable. Emotional ups and downs preclude this. Consequently, I never gave rah-rah speeches or contrived pep talks. There was no ranting or raving, histrionics or theatrics before, during, or after practice and games.’

‘I wanted to conduct myself in a manner that would not reveal to an observer whether UCLA had outscored an opponent or not. Even my dear wife, Nellie, said she couldn’t tell from my expression.’

John Wooden’s 10th NCAA Title 1975 [source AP]

‘Emotional control is a primary component of consistency, which, in turn, is a primary component of success.’

‘I wanted to see fervour during UCLA basketball practice and games, intensity that didn’t boil up and over into emotionalism.’

‘Good judgement, common sense, and reason all fly out the window when emotions kick down your door.’

‘Emotionalism - ups and downs in moods, displays of temperament - is almost always counter-productive, and at times disastrous.’

‘My teaching stressed that ‘losing your temper will get us outplayed because you’ll make unnecessary errors; your judgement will be impaired.’ I didn’t mind an occasional mistake unless it was caused by loss of self-control.’

Marginal Gains

‘You have to apply yourself each day to becoming a little better. By applying yourself to the task of becoming a little better each and every day over a period of time, you will become a lot better.’

Tone at the Top

‘Your own example counts most.’

‘I believe there is no more powerful leadership tool than your own personal example. In almost every way the team ultimately becomes a reflection of their leader.’

‘The leader’s attitude, conscious and subconscious, inevitably becomes the attitude of those he leads. Winston Churchill’s resolution, courage, and defiance nourished an entire nation in the worst of times; his attitude became the attitude of those he lead. The same things happens with effective basketball coaches and business leaders.’

‘As a leader, you must be filled with energy and eagerness, joy and love for what you do.’

‘As leader, my behaviour set the bounds of acceptability. And letting emotions spill over onto the court was simply unacceptable.’

Leaping Emergent Effects

‘Team Spirit - an eagerness to sacrifice personal interests or glory for the welfare of all is a tangible driving force that transforms individuals who are ‘doing their jobs correctly’ into an organization whose members are totally committed to working at their highest levels for the good of the group. When this happens and the leader is the one who makes is happen - the result is almost magical.’

‘A leader can get the unseen potential of individuals to blossom when she or he leads the entire team and not just the star players. This type of leader creates an environment in which every job matters and every member of the organisation counts. In this atmosphere, everyone know the team’s success rests, in part, on their efforts to seek personal greatness.’

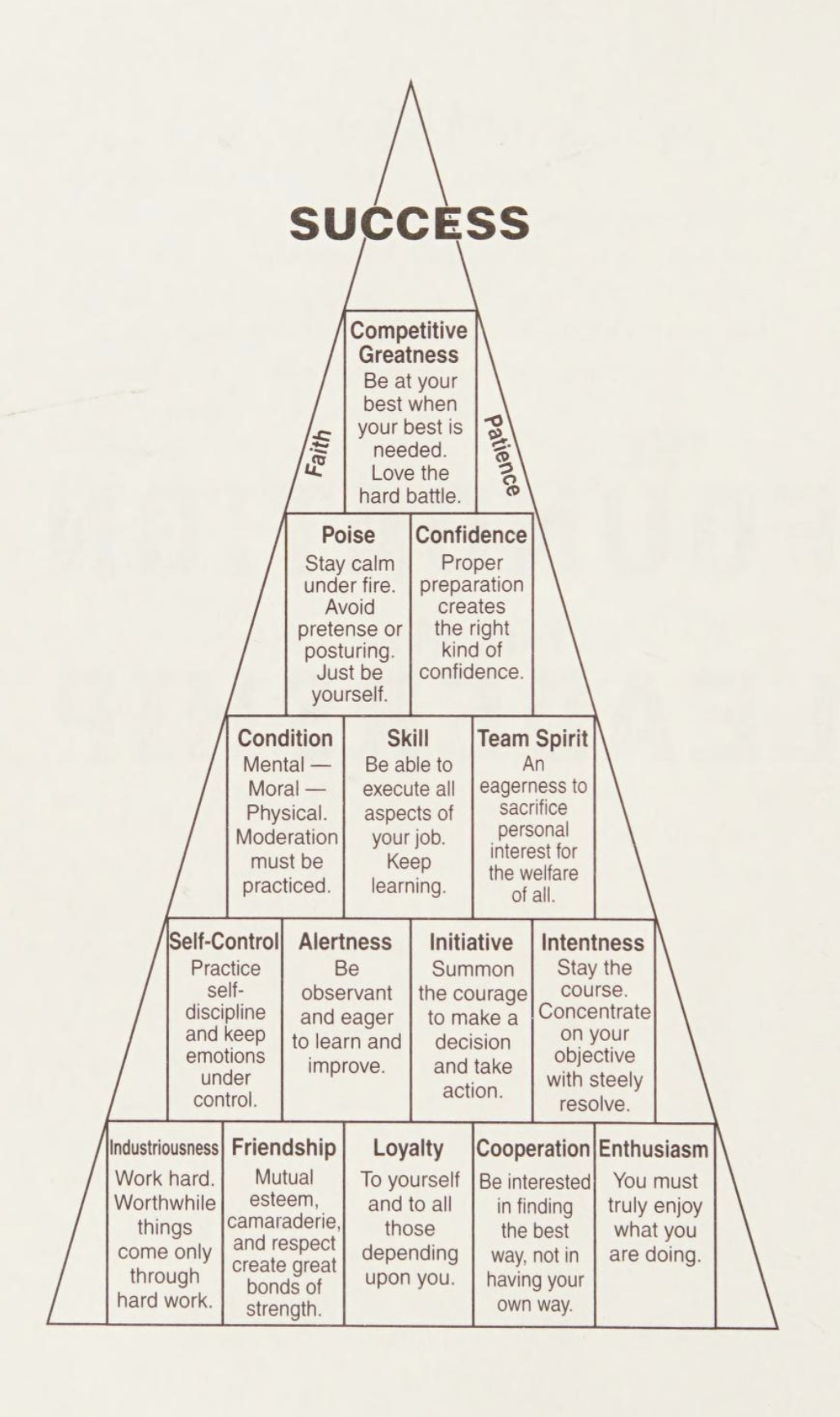

Pyramid of Success [Wooden on Leadership]

‘Each member of your team has a potential for personal greatness: the leader’s job is to help them achieve it.’

‘An organization that has all members focused first and foremost on doing what benefits the group is a force to be reckoned with. I know personally what can happen when everyone truly believes it takes 10 hands to make a basket.’'

‘Team spirit has the potential to increase the productivity of you organisation exponentially; Your team becomes greater than the sum of its players; the organisation greater than the number of employees on its payroll. Each individual revels in the glory of the group rather than the glory of the individual. ‘What can I do to help our team today’ replaces ‘How can I get ahead?’ (of course, I believe the answer to the latter is found in the former.)’

‘Some individuals are more difficult to replace than others, but every person contributes - or should - to overall organizational success. Each individual must feel valued, from the secretary to the superstar salesperson and the senior manager. And, above all, each person must comprehend precisely how his or her own job performance is linked to the team's welfare and survival. When this is accomplished, you have made each one feel a part of something much bigger than her or his individual job.’

‘A team filled with people striving to reach 100 percent of their potential in ways that serve the team becomes a force with exponential power and productivity.’

‘A leader or who can get the unseen potential of individuals to blossom when she or he leads the entire team and not just the star players. This type of leader creates an environment in which every job matters and every member of the organisation counts. In this atmosphere, everyone knows that the team’s success rests, in part, on their efforts to seek personal greatness.’

Team

'The star of every successful team is the team. Individuals don't win games, teams do.’

‘There is only one star that counts: the team.’

‘A player who is more concerned with his or her own statistics rather than those of the team is a player I welcome on the opponent's side of the court. The presence of such an individual weakens the team and makes it vulnerable during competition to a disciplined group filled with Team Spirit.’

‘Team Spirit is one of the most tangible ‘intangibles’ I have ever encountered. It's difficult to see; you feel it. And it's a powerful feeling for an organization to have.’

‘Getting your people to think ‘Team First’ is vital. It starts when you teach each member of the group how she or he contributes to the organization, when you make each one feel connected to the team's efforts, productivity, and ultimate success.’

‘Whether in business or in basketball, no superstar or top performer, regardless of his or her level of God-given talent and productivity, does it alone. Every basket Bill Walton ever made utilised ‘10 hands.’ In truth, it involved many more than 10 - the hands, the heads, and hearts of nonstarters, the assistant coaches, the trainer, the managers, and of course, the coach.’

‘‘Ten Hands’ was one of the most important principles that a player or employee can be taught... my own firm belief is that a player who made the team great is better than a great player.’

‘‘For the strength of the pack is the wolf; and the strength of the wolf is the pack.’ That describes the relationship between the individual and the organization - the player and the team.’

‘A player who is thumping his chest after he makes a basket is acknowledging the wrong person. Thus, I insisted the player who scores gives a nod or ‘thumb’s up’ to the teammate who helped - the one who provided the assist. That way it was more likely to happen again.’

‘By insisting that the scorer acknowledge others, I was strengthening the connection those ‘others’ felt to the production process.’

‘It takes 10 hands to make a basket. Don't just reward the two hands scoring points. Recognize the additional hands that make the points possible. They are crucial underpinnings of a winning organization.’

Recognition and Incentives

‘Sharing credit is a surefire way of improving the performance results for any organisation. Everyone starts helping everyone.’

‘When choosing between the carrot and the stick as a motivational tool, the well chosen-carrot was almost always more powerful and longer lasting than the stick.’

‘Conventional carrots include money, of course, as well as advancement, awards, a corner office, or a more prominent role in the team or in the organisation. Carrots come in many forms. However, I believe the strongest and most meaningful motivators are not necessarily the materialistic, but the intangible. In this regard, there is perhaps no better carrot that approval from someone you truly respect, whose recognition you seek. Acknowledgement, a pat of the back, a wink, a nod of recognition or praise from someone you hold in high esteem is most powerful - the most valuable carrot of all. At least, this has been my experience.’

‘Dictator-style coaches and leaders have their own approach (all sticks, no carrots) and can also rise to great heights. But for me, the fear and ill feelings that arise from intimidation, punishment, and cruel words have far less power than pride.’

Caring and Family

‘I believe most people, the overwhelming majority of us, wish to be in an organization whose leadership cares about them, provides, fairness and respect, dignity and consideration.’

‘For a parent, the family counts most of all; for a good leader, the team is nothing less than extended family. Those you lead are not just a random collection of people who show up at your doorstep, put in time, and collect a paycheck. At least, they shouldn't be.’

‘For me the members of our teams were never plug-in parts, ‘jocks’ whose individual value was in direct proportion to the number of points they could score. Never. In fact, next to my own flesh and blood they were the ones closest to me. Those I led were my extended family. And love is present in every good family. You must truly care about the lives and welfare of your team members, and demonstrate it with concern and support within a disciplined environment.’

‘A team - your organisation - is a family. Love must be the glue that holds it together, and love must start with the leader.’

‘Success is much more likely when love is present in your heart for the people who make you organisation a real team, that is, a family.’

‘Teams with a sense of family have uncommon strength and resiliency.’

‘The small considerations often mean the most - a genuine expression of interest or concern, a helpful hand, individual recognition. I knew about players families and their challenges away from basketball. Oftentimes, it really is the thought that counts most.’

New Ideas and Listening

‘Being an effective leader – one who can build a winning organisation – requires being an effective listener. The most productive leaders are usually those who are consistently willing to listen and learn.’

‘New ideas and perspective from those under your leadership are essential for achieving and maintaining a competitive edge. Welcome those people strong enough to speak up and offer alternative ideas.’

Source: ASUCLA

‘An effective leader understands that it is a sign of strength to welcome honest difference and new ways of thinking from those on your teams as well as from others. Progress is difficult when you won’t listen.’

‘The best leaders are more interested in finding what’s right than in always being right. They understand how much more can be accomplished if no one cares who gets the credit.’

‘I don’t need ‘yes men.’ If they’re going to yes everything I do, I don’t need them around.’

Change

‘Seek significant change. Be uncomfortable being comfortable, discontent being content.’

‘My philosophy of leadership stood me in good stead during nearly half a century in the competitive arena, and, in spite of all of the changes we see around us, I believe it can be equally effective in the twenty-first century. Some things don't change. Some rules remain the same.’

Learning

‘The path to success lies in the realisation that there is always more to learn. Strive to create an environment where individuals continually seek knowledge that will benefit their team, where you and those in the organisation aren’t afraid to ask questions - to admit, ‘I don’t know’’’

‘Of course, knowledge is never static or complete. A leader who is through learning is through. You must never become satisfied with your ability or level of knowledge. Subsequently, after each season I picked one particular aspect of basketball to study intensively.’

‘The best CEOs are often those credited with developing ‘learning institutions.’ Take meaningful steps to make this a reality. Invite managers from other companies to speak to your people on a key topic. Encourage others to take relevant courses and, most of all, lead by example; specifically, let those you lead see their leader continually learning.’

‘I draw inspiration and direction from a wide array of sources, including my father, Coach Ward Lambert, Abraham Lincoln, Mother Teresa and the Great Pyramid of Giza.’

Continuous Improvement

‘Success is not a destination, it is a journey.’

‘A good leader always seeks improvement - always.’

‘The best leaders understand that to successfully compete at any level requires continuous learning and improvement. Unless the leader communicates this up and down the line - and puts mechanisms in place to ensure it gets done - your team will not be 100 percent in its performance level.’

‘Never be satisfied. Work constantly to improve. Perfection is a goal that can never be reached, but it must be the objective. The uphill climb is slow, but the downhill road is fast.’

‘Accepting the status quo means a leader feels no further improvement can be made. I never reached a point in 40 years of teaching basketball where I felt no further improvement could be made. And that applied to every area of the game, including my own leadership skills.’

Self-Control

‘Self control in little things leads to control of bigger things. For example, the reason I prohibited profanity - a small issue - during practices was because it was usually caused by frustration or anger… I believed and taught that a team lacking self-control will get boutplayed and, usually out-scored.’

‘In fact, as I watched a game unfold there would occasionally be an almost guilty pleasure in seeing our team exert enough pressure to cause the opponent to lose control. I never wanted to see the situation reversed.’

Complacency

‘Success breeds satisfaction; satisfaction breeds failure. A leader must set realistic goals, but once they are achieved, you must not become satisfied. Achievement will continue at the same or a greater level only if you do not permit the infection of success to take hold of you and your organization. The symptom of that infection is called complacency. Contentment with past accomplishments or acceptance of the status quo can derail an organization quickly. In sports or business, getting to the top is difficult. One of the reasons staying there is so rare is because the infection sets in.’

Do the Right Thing

‘Character - doing the right thing - is fundamental to successful leadership.’

‘Good values are like a magnet - they attract good people.’

‘Aristotle said: ‘We are what we repeatedly do.’ He was referring to character - the values and habits of our daily behaviour that reveal who and what we are. I wanted to create good habits in those under my leadership, not only in the mechanics of playing basketball, but also in the fundamentals of being a good person. Thus, a small issue such as putting towels in the towel basket where they belonged was something I viewed as big, something that connected to my overall principles and beliefs -values that went beyond just picking up after yourself.’

Appearances

‘I insisted that jerseys always be tucked in, because I felt it helped create a sense of self-identity and unity. It was a detail that helped teach our players that sloppiness was not tolerated - in anything. Eliminating sloppiness and creating unity were very important to me and were effectively instilled by attending to such details.’

‘From the minute a UCLA Bruin put on a UCLA uniform - even a practice uniform - I wanted him to recognize that he was now part of something special, an organization, a team, a group that did things differently. And it did things the right way all the time, starting from the ground up.’

Mentors

‘Mentors are available at all stages of your leadership life; absorb their knowledge and use it.’

Transparency

‘Insist that Members of Your Team Share the ‘Ball’ - Information, Ideas, and More. The most effective leaders understand the importance of making sure that no member of the team hoards data, information, ideas, and the like. In business, it is the sharing of ideas and putting them to work that leads to a ‘best practice’ mindset.’

Cross-Training

‘Sometimes during practice Coach Wooden would have the guards switch positions with the forwards have us do the other guy's job. He wanted everybody to understand the requirements of the player in the other positions. Coach Wooden wanted the guard to appreciate the challenges a forward faced and the forward to appreciate what a guard had to deal with.’ Gail Goodrich

‘Whether in basketball or business, you must be able to perform all aspects of your job, not just part of it. You must be able to ‘get open’ and ‘shoot'. One without the other makes you a partial performer, someone who can be replaced because your skills are incomplete.’

Listening & ‘Yes-Men’

‘Surround yourself with people strong enough to change your mind.’

‘Being an effective leader, one who can build a winning organization - requires being an effective listener. The most productive leaders are usually those who are consistently willing to listen and learn. New ideas and perspective from those under your leadership are essential for achieving and maintaining a competitive edge. Welcome those people strong enough to speak up and offer alternatives and ideas.’

‘John Wooden did not want "yes men" around him. We were encouraged to argue our points, knowing he'd come back at us strong with his own opinions.’ Gary Cunningham

Repetition

‘John Wooden always used the laws of learning: explanation, demonstration, imitation, and repetition. Lots of repetition. You can't believe the repetition.’ Gary Cunningham

Resilience and Crisis

‘Adversity can make us stronger, smarter, better, tougher. Blaming your troubles on bad luck makes you weaker. Most worthwhile things in the competitive world come wrapped in adversity. Good leaders understand this.’

‘When the going gets tough, the tough get going. Don't beg, cry, alibi, sulk, or lose your self-control; but do maintain poise, condition, alertness, confidence, industriousness, enthusiasm, fight, and desire.’

‘Although you may not be able to control what fate brings your way, you can control how you react and respond to it. At least, you should be able to.’

‘Walt Disney once said, ‘There is no education like adversity.’ However, to gain this education you must be tough enough to overcome adversity rather than allowing adversity to overcome you.’

Optimism

‘I don't know exactly why, but I began accepting what fate offered and tried to make the best of the situation to move forward with optimism and the determination to make the most of the hand I was dealt, whether it was good or bad.’

‘Be a realistic optimist and remind yourself that things turn out best for those who make the best of the way things turn out.’

‘Always believe there is a positive to be found in the negative. Things usually happen for a reason, even when you are unable to discern the reason.’

Trust

‘When you say you'll do it, do it. Don't give your word unless you intend to keep it. A leader whose promise means something is trusted. Trust counts for everything in leadership.’

Checklists

‘When I was coaching, I had a pretty good memory for facts and figures, names and faces, and the rules of behavior that members of the team were expected to follow. Nevertheless, I wrote things down, including lists of personal qualities that I wanted our players to have or develop the ingredients necessary for a successful team. While my memory served me very well, I took no chances that something would be overlooked or forgotten. Lists. Lots of lists resulted.’

Unconventional

‘The 1961-1962 season would be a turning point for UCLA basketball, one that eventually produced 10 NCAA championships including seven in consecutive years and an 88-game winning streak. I had no idea it was all about to happen.

Starting in 1962-1963, my new policy was to go primarily with seven main players virtually, seven starters in both practice and games. My previous goal of doling out playing time in a democratic manner was discarded. I changed a fundamental policy for how I did things.

I didn't intend to ignore the eighth to twelfth players, obviously, but I let them know very clearly what their roles in the group would be and for what purpose. More important, I tried very hard to make them understand the great value of their role and how it would contribute to the overall welfare of the team. In part, this meant they would be the stone that sharpened the sword, that is, the starting lineup.’

‘One of the challenges I faced with the Bruins during practice was dealing with the distraction caused by a player's natural instinct and desire to score baskets or grab rebounds. I attempted to solve this particular problem at UCLA by occasionally removing the siren song; specifically, I made them practice and play basketball without the ball. Without the basketball, player can neither score baskets nor grab rebounds. Without those distractions, he was better able to fully concentrate on what I was teaching.’

‘I would never retire a player's number, because it suggests that a single individual is the greatest to ever wear it. Retiring the number in their name dismisses the great effort and contributions of all others who have worn that same number.’

‘I also used a somewhat unusual approach in helping individuals learn correct habits the fundamentals - for rebounding. Again, it stemmed from my desire to use time as efficiently as possible. Obviously, it's difficult to practice rebounding if there's no rebound -if the shot goes through the hoop. Thus, at times we practiced rebounding with a cover over the basket, which meant that every shot produced a rebound opportunity.’

‘When it came to perfecting details I worked ‘feet first,’ from the ground up. Socks? During our first team meeting I personally showed players how to put them on properly. Shoes? We didn’t ask players what size they wore. I insisted our trainer measure each student-athlete’s foot - to ensure that newly issued sneakers fit properly. I wanted no slippage.’

Legacy

‘A leader truly dedicated to the team's welfare doesn't make himself irreplaceable. Things did not fall apart just because I was gone.’

‘Who are your assistant leaders? Are you allowing them the opportunity to learn and grow as leaders? Is there someone ready to take the reins of leadership in case something happens to you? Or do you feel threatened by having someone in the organization potentially be your replacement?’

Summary

At first glance, basketball and business may appear worlds apart, yet the traits that defined the greatest college basketball coach, John Wooden, echo in the triumphs of the world's most successful businesses. Wooden was a fanatic. He realized that while perfection was unattainable, striving for it ensured the team produced at the highest levels. He took emotion out of the game, something as relevant for sporting success as it is for business and investment.

Nurturing his players, instilling autonomy, embracing unconventional methodologies, fostering a culture steeped in integrity and respect, and establishing a top-down leadership tone comprised essential elements of his triumph. Acknowledging every team member, integrating them into the mission, and acknowledging their successes triggered emergent effects, where the collective impact surpassed individual contributions. In the business landscape, akin to a basketball team, an organization is an assembly of individuals. Employing strategies to unlock each person's potential yields extraordinary outcomes. This understanding, exemplified by John Wooden, is a shared ethos among exceptional CEOs who recognize the transformative power of cultivating a unified and empowered team.

Source:

‘Wooden on Leadership,’ John Wooden and Steve Jamison. McGraw-Hill. 2005.

Further Material:

‘Ted Talk - The difference between winning and succeeding,’ John Wooden, 2001.

Follow us on Twitter : @mastersinvest

* Visit the Blog Archive *

TERMS OF USE: DISCLAIMER