A recent post by John Hempton of Bronte Capital on a fairly well known value investor's portfolio back in March 2008 posed the challenge of 'risk-assessing' the portfolio. I don't know Mr Hempton personally but I enjoy reading his posts, he's an independent thinker.

The post, titled "A puzzle for the risk manager", detailed the investment manager's stock portfolio which performed very poorly over the next 12 months. Managing assets requires continued learning and you can learn a lot by studying not only your own mistakes but the mistakes of others.

"The big difference between those who are successful and those who are not is that successful people learn from their mistakes and the mistakes of others" Sir John Templeton

This case study provides a great opportunity to think about the process of portfolio construction, human psychology and history.

Here is the portfolio:

I'll run through some of my thoughts on the portfolio and the issue of portfolio construction.

The key to managing risk is to think. There is no substitute for thinking about the portfolio and how it may perform in adverse conditions. Using screens and computer models of loss expectancy are a poor substitute for common sense and many fund managers who relied on such models learnt an expensive lesson in the financial crisis.

“The best way to minimize risk is to think” Warren Buffett

"In life as in investing, what kills you is what you don't know about and what you're not thinking about" Bruce Berkowitz

The number one risk a portfolio manager must avoid is the permanent loss of capital. So the question becomes, does this portfolio pose the risk of the permanent loss of capital?

Building an investment portfolio involves a lot more than just picking cheap stocks. It requires consideration of position sizes, industry concentration, liquidity and how the overall portfolio will perform under different scenarios including those which may not have happened before. The portfolio manager must be alert and aware of changes in the markets, economy, politics, and society at large. Changing circumstances may warrant portfolio changes.

In many cases, portfolio failure results from poor portfolio construction, a failure to recognise changing circumstances and/or the failure of imagination about what the future may portend.

A portfolio must be constructed to withstand the unexpected.

"A fiduciary should think more about the safety of an entire portfolio than about any individual holding" Seth Klarman

In assessing any portfolio, I like to think of the seven common causes of catastrophic failure - excessive concentration, excessive correlation, illiquidity, excessive leverage, fraud, capital flight and valuation risk.

Let's assess the subject portfolio on each:

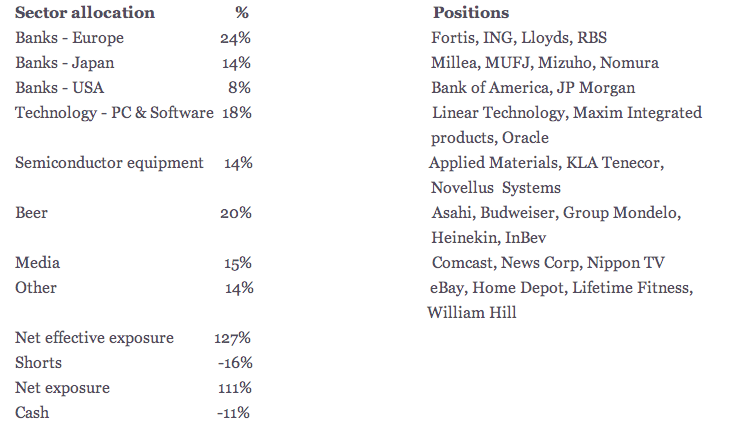

Concentration: The subject portfolio has 48% of its assets exposed to the financial sector. To me this is the biggest risk as financial stocks inherent leverage make them susceptible to failure.

While Warren Buffett has invested in financials he also acknowledged the significant risks. His 1990 letter referenced his Wells Fargo investment that year...

"The banking business is no favourite of ours. When assets are twenty times equity - a common ratio in this industry - mistakes that involve only a small portfolio of assets can destroy a major portion of equity. And mistakes have been the rule rather than the exception at many major banks."

Mr Buffett thought broadly about the possible worst case scenarios facing both the banking sector and Wells Fargo. Only after concluding such a worst case outcome would not 'distress him' did he invest.

"Of course, ownership of a bank - or about any other business - is far from riskless. California banks face the specific risk of a major earthquake, which might wreak enough havoc on borrowers to in turn destroy the banks lending to them. A second risk is systemic - the possibility of a business contraction or financial panic so severe that it would endanger almost every highly-leveraged institution, no matter how intelligently run. Finally, the market's major fear of the moment is that West Coast real estate values will tumble because of overbuilding and deliver huge losses to banks that have financed the expansion. Because it is a leading real estate lender, Wells Fargo is thought to be particularly vulnerable. None of these eventualities can be ruled out."

Buffett noted at the time..

"Buying into the banking business is unusual for us.. but opportunities that interest us and that are also large enough to have a worthwhile impact on Berkshire's results are rare. Therefore, we will look at any category of investment, so long as we understand the business we're buying into and believe that price and value may differ significantly."

The key point Mr Buffett makes here is "understand". The issue confronting investors prior to the financial crisis was that the banking industry had become increasing complex and opaque. Innovation in capital markets had seen credit markets grow feverishly as banks securitised significant quantities of assets, increasingly relied on wholesale funding markets as opposed to deposits, played in credit derivatives and placed excessive trust in ratings agencies. The global banking industry had become far more entwined and far more susceptible to fickle credit markets.

“Complex systems are full of interdependencies—hard to detect—and non-linear responses. In such an environment, simple causal associations are misplaced; it is hard to see how things work by looking at single parts. Man-made complex systems tend to develop cascades and runaway chains of reactions that decrease, even eliminate, predictability and cause outsized events. So the modern world may be increasing in technological knowledge, but, paradoxically, it is making things a lot more unpredictable.” Nassim Taleb

"The condensation of credit cycles and the increasing incidence of credit dislocations is a consequence of the globalisation of the world economy, technological advancements in the electronic transmission of information, and financial innovations such as derivatives and securitisation that blur the distinctions among markets and asset classes. The confluence of these developments has perversely made the markets more informed but less informative. Information and capital rocket around the world at unprecedented velocities and volumes, leaving investors to process market data before reacting. Today, a pin dropping in Argentina can cause simultaneous ripples (or waves, or in rare cases tsunamis) as far away as Japan. By the time the pin drops, it may already be too late for investors to protect their capital. In a financial world dominated by innovation and new products that blur the traditional distinctions between debt and equity, disruptions in the credit markets are certain to affect all hedge fund strategies in all asset classes. The increasing frequency and severity of extreme credit events points to the heightened risk of contagion among markets and asset classes. " Michael Lewitt, 2003

It's hard to see how an investor could have had a reasonable understanding of the risks sitting on the books of many of the global banks. Increasing reliance on credit markets posed risks, even for those banks with large deposit bases. An investor with a generalist mindset and an appreciation of credit markets would be mindful of the potential for capital destruction in the sector.

"The analysis of credit cycles involves an understanding of monetary policy, financial and industry innovation, and regulatory change. The ability to identify in advance those moments when credit cycles veer into crisis also requires imagination, an appreciation of human folly and a willingness to imagine worst case scenarios. In order to identify times of maximum risk, understanding human psychology is at least as important as understanding economics. Credit cycles involve a combination of historical, sociological, political, economic and psychological factors that are both unique to each specific cycle and common to all cycles. Hard and soft data must be examined. The unhappy truth is that markets don't learn their lessons very well. Financial history tends to repeat itself. The only questions are when and to what degree. Hedge fund managers charged with preserving capital and producing positive returns in both good and bad markets must pay particular attention to the etiology of credit cycles and particularly those extreme turning points that lead to financial crisis that can consume years of returns in the blink of an eye" Michael Lewitt 2003

The world's best investors take account of the fact that some things cannot be known. Forecasts are often wrong. Investors make mistakes. Portfolios must be constructed to account for these limitations.

"We adhere to policies that will allow us to achieve acceptable long-term results under extraordinarily adverse conditions, rather than optimal results under a normal range of conditions" Warren Buffett

"A small chance of distress or disgrace cannot, in our view, be offset by a large chance of extra returns" Warren Buffett

"We should all be humble enough to realize that once every 20 or 30 or 40 years, values go to real extremes. Any investment program must take into account the impossibility of knowing when and to what extent such extremes might occur." Paul Singer

While most successful investors run reasonably concentrated portfolios they diversify across industries in an attempt to limit downside risk, no matter how favourable one particular sector may look.

"We have had periods in which one or more areas looked absolutely fabulous, but it is part of our discipline to continue to invest in a number of areas in order to limit pain if we are wrong about any one" Paul Singer

The subject portfolio had 26% of investments exposed to the tech sector [technology/semiconductor], 20% in beer investments and 15% in media assets. Industry exposure limits must be set relative to the potential risk, however a 20% limit is common amongst successful investors.

Correlation - It's not hard to see the significant risks a US recession/credit dislocation would pose on this portfolio given the increasing systemic risk in the global banking industry.

A global recession would also place pressure on consumer spending and business capex. In times of turmoil correlations have a tendency to go to one. So without hedges or cash, portfolios can be at risk of significant loss. The key is ensuring they are not permanent.

"If every position in the portfolio could be uncorrelated with every other position and also uncorrelated with the markets, we would be happy indeed. However, as the world does not work that way, we approach diversification and seek uncorrelation in an incremental fashion." Paul Singer

"Hidden fault lines running through portfolios can make the prices of seemingly unrelated assets move in tandem. Correlation is often underestimated, especially because of the degree to which it increases in crisis. A portfolio may appear to be diversified as to asset class, industry and geography, but in tough times, non-fundamental factors such as margin calls, frozen markets and a general rise in risk aversion can become dominant, effecting everything similarly." Howard Marks

Establishing a checklist of risk factors that may negatively impact a portfolio and then calculating the percentage exposure can assist in identifying fault lines and downside risk in the portfolio. Risk factors such as sector/industry exposure, market cap, liquidity, inflation, high gearing, interest rates, currency, housing market exposure, recession, market leverage/beta, consumer exposure, business capex, high PE, business quality, yield, credit market, index type, investor crowding, disruption, cyclical/defensive, growth/value, sovereign/geographic exposure etc are a good starting point.

Building protection through cash holdings or hedges can limit portfolio risk. The cost of such hedges maybe under-performance in a bull market. This is a cost successful investors are prepared to accept.

Liquidity - Liquidity is important as it allows the manager to exit in case of a faulty or changed investment thesis or in the event of redemptions [capital flight]. Illiquidity and redemptions can be a deadly combination. It would appear the subject portfolio was liquid enough to allow the manager to reduce losses before they became catastrophic.

Capital Flight - Any fund manager that experiences significant losses or relative under-performance is at risk of redemptions depending on the nature of the end client. A portfolio may experience significant mark to market losses even while the intrinsic value of the stocks are little changed. While volatility is ordinarily the friend of the value manager, in time of market chaos the manager may not get the opportunity to ride out the market decline should significant redemptions arise. The issue for the subject portfolio is that the mark to market losses reflected permanent loss of capital which impeded a recovery.

"I may not care about volatility but the reality of having temporary capital is the volatility matters" Mohnish Pabrai

Leverage - This subject portfolio had debt at two levels, the stock level and the portfolio level. The risk inherent in the financials positions was discussed above.

The subject portfolio had long exposure of 127% and a short position of 11% providing a net exposure of 111%. This means that for every $1 invested by a fund unitholders, the manager had $1.11 exposed to the market. While not ridiculously aggressive, I personally don't understand why managers run net exposures over 100%. Many long only fund managers mandates limit cash holdings which poses the question "who is making the call on whether the market is attractive?". It appears this manager had the ability to run lower net and chose not to. If you are going to run a short book I think it makes sense to use it to minimise portfolio risk not increase it. The subject portfolio is no different to a geared long fund [absence any commentary on the shorts? ie high beta?].

Valuation Risk - Mr Hempton noted the "PE ratios mostly looked reasonable". On a "screening process" the portfolio probably looked attractive relative to the market. At the time, the market was elevated and a M&A frenzy was driving stock multiples higher. A 'value screen' at the time would take no account of the fact bank earnings were about to collapse [with the benefit of hindsight] and a low PE was no protection from a credit dislocation. The banks were 'value traps'.

Fraud - while there is unlikely to be a case of fraud by the manager there was certainly fraud going on at the US housing level.

Ultimately the subject portfolio failed as it wasn't constructed to handle a credit crisis. The portfolio's financial investments did not recover like the broader market due to bank recapitalisations, bankruptcies or nationalisations. There was permanent loss of capital.

Other value managers faced severe drawdowns through the crisis but provided they had more permanent capital and/or liquid positions and their portfolio's intrinsic value wasn't impaired they could hold on for the market price to better reflect the underlying value of the stocks. Owning, high quality businesses, with good cash flow and solid balance sheets allowed many investment managers to recover quickly from the market sell-off of 2008/2009.

"People don't believe business quality is a hedge, but if your valuation discipline holds and you get the quality of the business right, you can take a 50 year flood, which is what 2008 was, and live to take advantage of it" Jeffrey Ubben

The chart below shows a portfolio containing an equal weighting of the subject portfolio's stocks which is a reasonable proxy for the subject portfolio [in white]. It highlights the subject portfolio's performance mirrored the S&P500 and FTSE Banks indices [a good reason sector ETF's aren't safe! but that's another topic]. These indices experienced significant permanent losses and never recovered like the broader market.

Some additional thoughts ..

History - the 2008/2009 global financial crisis wasn't the first time the banking industry had suffered serious losses. Had the manager considered previous credit crisis it's unlikely he/she would have had such an aggressive exposure to banks. There were plenty of warning signs a crisis may be coming.

Macro - the portfolio manager appears to have picked the portfolio on the basis of cheap stocks with little consideration of the macro risks. Plenty of value managers who considered themselves 'stock pickers' paid dearly for ignoring the macro environment in 2008/2009.

Humility - there is every possibility the manager had a track record of success in the bank sector before which blinded him/her to the potential dangers.

"There’s this balancing act between being stoic and an investor who’s maybe too ashamed to admit they’re wrong or in denial about being wrong. It’s a risk. If you’re so used to being right in the end, and if you’re used to your investment thesis working out “Sometimes the difference between success and failure was not just about our understanding and steadfast belief in the value of a holding, but how long we were willing to wait to achieve that result. In the long term, you can always lull yourself into a sense of complacency that everything will work out and that if you seem wrong today, you just wait a little while and you’ll be proven right. It can be a problem to trick yourself into believing too much in your own capabilities, if you are overly patient without being as discerning about whether it’s justified or not." Chris Mittleman

Social Proof - Mr Hempton noted "all of these positions could be found in quantity in the portfolios of other good investors." The portfolio manager may have taken comfort from this. While it can be useful to look at other investors holdings it doesn't abdicate the requirement for independent thought and analysis. Other investors portfolios may have been constructed with less risk or hedged. Other 'good' investors may be wrong.

"You are neither right nor wrong because the crowd agrees or disagrees with you. You are right because your data and reasoning are right." Warren Buffett

“In every great stock market disaster or fraud, there is always one or two great investors invested in the thing all the way down. Enron, dot-com, banks, always ‘smart guys’ involved all the way down.” Jim Chanos

Losses - while the portfolio was under pressure I'd argue the manager had the opportunity to significantly reduce risk to minimise losses. The chart below shows the portfolio was down c20% at the time the UK lender Northern Rock collapsed after the European credit markets closed shut. Given the exposure to European Financials this should have flashed a warning sign. The manager had liquid positions and the ability to cut losses.

A Portfolio manager's judgement can be impaired by losses and it can be difficult to implement hedges/risk reduction in a crisis. It's important to constantly review the portfolio, test your investment ideas, remain intellectually honest and address mistakes.

“The price of managing risk in the middle of a crisis is much too high so we try position the portfolio to thrive in a variety of market environments” Jake Rosser

"Large losses, though initially only on paper, often derail an otherwise rational investor. An illogical fear of loss insidiously exerts an undue influence on portfolio decision making. (Rationally, the lower prices go, ceteris paribus, the less the likelihood of further loss—a truism that falls on deaf ears when fear has the upper hand.)" Frank Martin

While this portfolio manager may have had a track record of success prior to 2008 the permanent loss of capital was significant. As they say in this business, you're only as good as your next trade. Unfortunately, a solid track record of success can be eliminated by the permanent loss of capital. Never forget, any number times zero, is zero!

"In business and also investment, success is measured through the compounding of a series of returns. Mathematically, the biggest risk to a compounded series of returns is large negative numbers or even a single negative number, if large enough. Take however many spectacular annual outcomes and multiply them by just one zero and the answer is of course, zero" Marathon Asset Management

Further Recommended Reading-

One of the best articles on risk management is 'Risk Control & Risk Management' by Paul Singer of Elliott Associates, whose 35 year-plus track record of consistent returns with only two small down years is astounding. The article is featured in the book 'Evaluating and Implementing Hedge Fund Strategies', 3rd edition.

Michael Lewitt's essay "Understanding credit cycles and hedge fund strategies" forewarned of the risks in credit markets. The essay is also featured in the book 'Evaluating and Implementing Hedge Fund Strategies' 3rd Edition.

The excellent book 'Capital Returns' by Marathon Asset Management contains their prescient forewarnings of the risks building in the global banking system before it's collapse in 2008 and 2009.

The book 'Ubiquity - Why Catastrophes Happen' by Mark Buchanan delves into complex systems and how catastrophes can happen.

The Tutorials in the Investment Masters Class cover many topics relevant to the analysis and the links have been provided above.

DISCLAIMER