Picture two people standing in the same restaurant, watching the same rival open across the street.

In the first version, you own the place. A competitor selling the same food has just set up shop across the road, and it feels personal — a threat to your money, your reputation, your family's future. You notice whether its tables are full. You study its menu. You watch its prices. You wonder what it's doing better, because your livelihood is tied to what happens inside your restaurant.

In the second version, you're the waiter working the same tables. The new restaurant barely registers. If anything, it's good news: one more employer bidding for your time.

An executive at AB InBev once used that contrast to explain how the company thinks about management, as recounted in Ian Cassel's Intelligent Fanatics Project: "Many companies inadvertently create waiters," he said. "We work tirelessly to create restaurant owners."

It's a simple story, but it captures something real about the businesses that keep outperforming for decades rather than years. Most companies say they want employees to think like owners — to care about waste, protect the brand, serve customers well, control costs, work together and make decisions for the long term. Then they pay them like hired hands, withhold the information owners would receive and deny them the authority to change anything.

The best companies see that contradiction and refuse to live with it. They don't merely tell people to act like owners. They give them a piece of the economics, a clear view of how the business works and enough authority to influence the result.

They create owners.

A Piece of the Action

The idea is not new.

In 1927, UPS founder Jim Casey offered shares in the company to key employees. At the time, employee ownership was unusual. Many large businesses were still run through rigid hierarchies, with capital at the top and labour at the bottom.

Casey saw something different.

"There is no bigger incentive than for someone to work for himself," he said when presenting the shares.

Employee ownership became one of the defining features of UPS. Drivers, managers and executives accumulated stakes in the company. The shares encouraged frugality, loyalty and attention to detail because each improvement belonged, at least partly, to the people making it.

Casey later described employee ownership as the principle that had contributed more than any other to building UPS. By the time the company prepared to go public in 1999, employees and retirees still owned roughly two-thirds of its outstanding shares. Every executive officer had more than twenty-five years of service and had accumulated a meaningful ownership position.

The ownership and the tenure reinforced each other. People stayed because they shared in the value being created. The longer they stayed, the more knowledge and ownership they accumulated. That knowledge helped create more value, which made staying more attractive still.

Publix developed a similar model. George Jenkins opened his first Florida grocery store in 1930 and built it into the largest employee-owned company in America — today more than 1,400 supermarkets and roughly 250,000 staff, with no public market in the stock. Jenkins wanted the people running the stores to participate in the profits they generated and in the value of the wider company. Full-time store employees share directly in the profits of their location, and Publix contributes a substantial portion of company profits to a retirement trust for eligible associates.

The arrangement did more than supplement wages. It gave employees a direct interest in whether shelves were stocked, customers returned, waste was controlled and the store prospered. As former Publix CEO Ed Crenshaw put it:

"When people have ownership of something, they do what it takes to improve the value of that ownership."

Publix doesn't call the people who work there employees. It calls them associates — or, as the company puts it, co-owners. That mindset sharpens under pressure. Crenshaw described what happens when a competitor opens nearby: sales take a hit, and because associates share directly in store profits, they feel that hit as well — which is exactly why they work harder to keep the customer in front of them.

Every thirteen weeks, Publix also pays out a fifth of each store's profits in cash directly to the people who work there, on top of the company-wide retirement trust. The incentive reaches all the way to the register, not just the boardroom. The result shows up in a number most retailers never get close to: Publix's annual voluntary turnover runs around 5 per cent, against an industry average nearer 65 per cent.

The pattern appears repeatedly across many of the world's best businesses. O'Reilly Automotive makes every employee a shareholder after six months. Wawa, Brown & Brown and Kiewit have each built their own versions of the same philosophy.

At Walmart, Sam Walton gave employees a financial stake in the company. By the time he wrote his autobiography, more than 80 per cent of Walmart associates owned shares directly or through profit sharing. Walton called it "the single smartest move we ever made." Not a new store format, not a distribution centre, not a purchasing system, but sharing the economics.

When the Factory Worker Becomes a Millionaire

One of the clearest modern examples is HEICO. For decades, the Mendelson family has used company stock in HEICO's retirement plan to spread ownership throughout the organisation. The opportunity is not confined to senior executives. It reaches factory workers, shipping clerks, technicians and administrative employees.

Laurans Mendelson spoke proudly about employees who became millionaires — and in some cases multimillionaires — because of the HEICO shares they accumulated. That result matters for reasons beyond personal wealth.

A factory worker who owns meaningful stock does not experience a quality problem in quite the same way as someone collecting only an hourly wage. A shipping clerk who participates in the company's long-term success has another reason to care whether an order arrives correctly and on time.

"They take a personal pride in being a HEICO team member," Mendelson explained.

The ownership tells employees something important: you are not merely a cost appearing in someone else's income statement. You helped create this value, and you deserve to participate in it.

Howard Schultz made the same point at Starbucks. Giving employees shares, he said, demonstrated that the company respected its people enough to share its success with them. That may be the deepest effect of broad ownership. It changes not only incentives but relationships. There is a difference between being told that people are the company's most important asset and being invited to share in the wealth they help create.

Share the Profits

Ownership does not always require publicly traded shares or a formal employee stock ownership plan. Sometimes the most powerful incentive is a direct share of the profits employees can personally influence.

Enterprise Rent-A-Car was built around that principle. Founder Jack Taylor believed managers should participate directly in the economics of the branch they operated. The logic was straightforward. Suppose an employee creates $100,000 of additional value and receives ten per cent, or $10,000. Suppose instead that the employee creates $1 million and receives $100,000. Which outcome should the owner prefer? Obviously the second.

"The more you make, the more the business makes," Taylor explained. "Why wouldn't I want that to happen?"

Yet many companies resist precisely that outcome. They worry about employees earning too much rather than asking how much value had to be created for those earnings to become possible. Taylor understood that a large employee bonus can be excellent news for shareholders when the underlying incentive is designed properly.

Barclay Simpson used a similar system at Simpson Manufacturing. Salaries were relatively ordinary, but employees could earn substantial bonuses when their branch performed well.

"If they have a really good quarter, they can get a ton of money," Simpson said.

He regarded that as a feature, not a problem. Employees became highly focused on branch profitability because their own compensation moved with it. The company also discovered that the arrangement created loyalty. Even when the financial crisis reduced sales and profits, most of Simpson's people stayed.

Les Schwab approached profit sharing with characteristic simplicity: "My thinking has always been, if I give away half the profits, I still have half left," he wrote. "If I share $10 million with people, I still have $10 million left." The point was not charity. Schwab believed sharing profits helped produce the profits available to be shared.

Lincoln Electric has applied the same philosophy for generations. A large portion of pretax earnings is placed into a bonus pool for employees. The system has survived recessions, industrial disruption and technological change because the reward is tied to productivity and long-term company performance. At Johnson Wax, S.C. Johnson reached the same conclusion: "I truly believe we are a high-performing company because of profit sharing. Our earnings are better because of it."

Keep the Incentive Close to the Work

Not every ownership plan works. A tiny amount of stock buried in a distant retirement account may have little influence on the decision an employee makes this afternoon. A company-wide bonus can feel equally remote when an individual has no idea how their work affects the final result. The strongest systems create a clear line between action and outcome.

Expeditors International does this through district-level incentives. Employees are rewarded according to the success or failure of the local district in which they work.

That proximity changes behaviour. Every shipment matters. Every customer interaction matters. Every unnecessary expense matters. Employees know their actions can influence the result and that the result can influence their compensation.

"How are we different?" former CEO Jeffrey Musser asked. "The employees of Expeditors treat the business as if it were their own."

The district structure makes ownership understandable. People are not being asked to improve the abstract earnings per share of a global corporation. They are being asked to improve a business they can see, serving customers they know, alongside colleagues whose work affects the same pool.

The old J.C. Penney partnership model worked in much the same way. Penney would first place a potential manager in a trial store. If the person demonstrated the ability and character to operate it successfully, they could become a partner with a one-third ownership interest. Before being permitted to finance an interest in another store, however, the manager had to train someone capable of replacing them. The system combined ownership, accountability and people development.

A manager could prosper, but only by building a store that prospered and developing another person capable of carrying it forward. The reward sat close to the result.

Ownership Without Shares

Literal equity is powerful, but some companies create an owner mentality even where employees do not own significant stock.

Vicki Tenhaken found the same pattern studying companies that had survived for a century or more. In Lessons from the Century Club Companies, she put it plainly: "Many of the Century Club companies engage in some type of profit-sharing, employee ownership, or participatory management practices. Even without any type of formal ownership, employees in these companies develop an ownership attitude – it's their company."

At Walgreens, Charles Walgreen encouraged store managers to think of themselves as independent retailers supported by a large organisation — not employees controlled by one. Store managers were close to customers, knew their local markets and had room to exercise judgment. The result was an unusually strong sense of ownership and remarkably low turnover among managers.

In-N-Out asks store managers to run each restaurant as though it were their own. Home Depot historically encouraged store leaders to tailor parts of the product range to local conditions. TopBuild tells field leaders to "Be the Owner." Amazon has made ownership one of its foundational leadership principles. Andy Jassy describes an owner as someone who asks: What would I do if this were my own money?

That behaviour cannot be produced by equity alone. It comes from authority — being trusted with real decisions — which managers tend to repay with the same pride, care and accountability an owner brings to something that is genuinely theirs.

A Stock Certificate Is Not Enough

Herman Miller understood that ownership had to be supported by something deeper. The company described three values attached to ownership: business literacy, equity and spirit.

Business literacy meant employees had both a responsibility and a right to understand the company. They needed access to the real situation — not vague encouragement or carefully managed corporate messaging. Equity meant sharing the positive and negative consequences of collective performance. Spirit meant commitment to the company, its goals and one another.

Herman Miller summarised the model in six words: "Innovation and excellence through participative ownership." The important word is participative. Ownership without information leaves people guessing. Ownership without authority creates frustration. Ownership without a meaningful economic stake becomes symbolic. Ownership without shared purpose can become individual greed.

Jack Stack discovered the same thing at SRC Holdings. After helping employees acquire an ownership stake, Stack taught them how the business actually worked. Workers learned to read financial statements, understand cash flow and see how inventory, pricing, productivity and collections affected the value of the company. The shares were only part of the system. People also needed to understand how that wealth was created.

"A company of owners will outperform a company of employees any day of the week," Stack said. Not because owners possess a certificate. Because ownership changes the way people notice, decide and act.

The Responsibility of Ownership

Ownership is often described as a reward, but it also creates responsibility. Max DePree of Herman Miller argued that owners cannot simply walk away from problems. Ownership increases accountability and demands maturity. It requires people to become more informed about the whole business rather than only their small part of it. That distinction matters.

Poorly designed incentives can produce the opposite of ownership. A sales commission may encourage someone to book a bad customer. A branch bonus may encourage underinvestment. Stock options can reward a rising market rather than genuine value creation. A distant company-wide target may encourage employees to assume someone else will carry the load.

The best systems balance reward with responsibility. They give people enough authority to act, enough information to judge and enough exposure to consequences to care. This is why employee ownership appears so frequently beside decentralisation, internal promotion and long tenure. The mechanisms reinforce one another.

A company promotes someone who understands the operation. It gives them responsibility for a branch, store or division. It lets them participate in the profits they create. The employee stays, develops judgment and accumulates ownership. Eventually, they teach the next person to do the same. The organisation compounds human capability alongside financial capital.

Ownership Polices Itself

There is a further benefit that rarely shows up on an income statement, though it quietly shapes one.

Brian Chesky has argued that the stronger a company's culture, the less corporate process it needs, because a strong culture means you can trust people to do the right thing without a rulebook standing over them. Herb Kelleher made the same point about Southwest Airlines: create an environment where people genuinely participate, and control becomes unnecessary, because they already know what needs to be done. The more people commit willingly, the fewer hierarchies and control mechanisms the business requires.

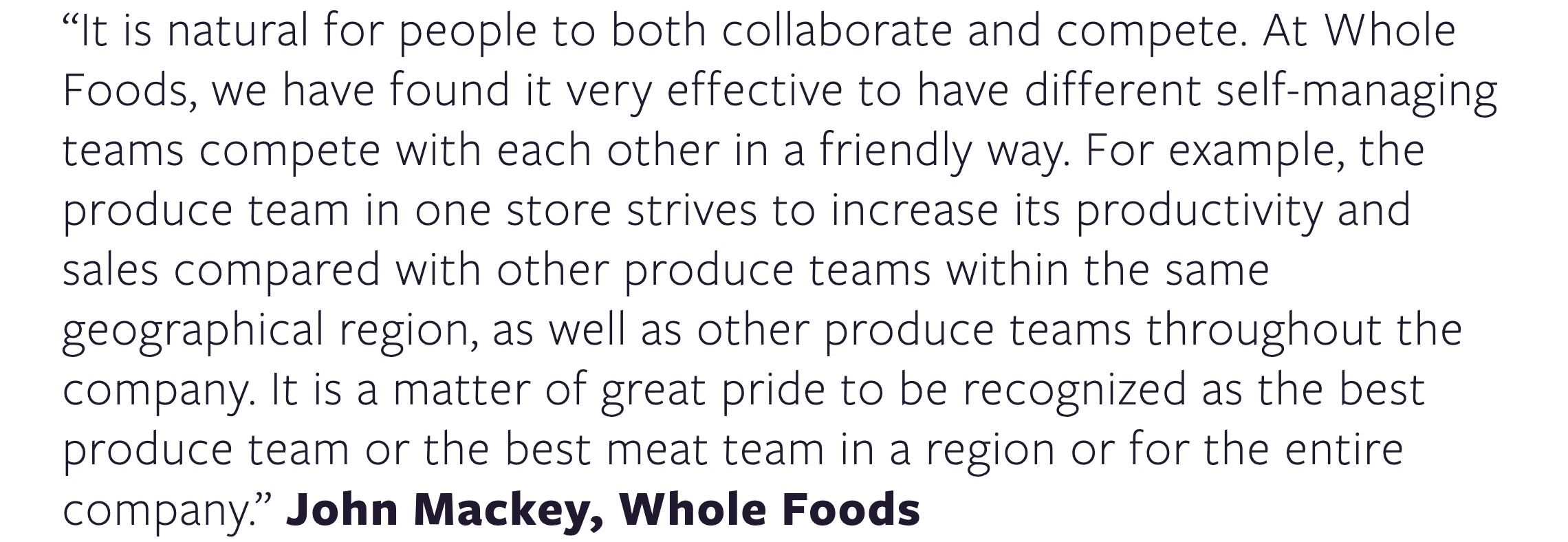

The effect is not only top-down trust. It is lateral pressure. Writing in the 1970s, the investor Phil Fisher observed that the pressure a peer group places on a tardy or lazy colleague dwarfs anything a manager could impose from above. John Mackey built Whole Foods around small, self-managing teams for the same reason: when every person's contribution is visible and everyone shares in the outcome, there is nowhere for a free rider to hide, because the team polices itself. Les Schwab saw it on his own shop floor — when pay was tied to shared results, a man dragging his feet heard about it from his own colleagues long before a manager had to step in.

Fred Reichheld described this as the underlying mechanics of partnership: a system in which everyone is motivated to create value together tends toward self-governance and self-correction. Partners do not need to be told what to do, because protecting the pool of value they all share is already their job.

For a public company, this shows up as leaner overhead — fewer layers of supervision, less need for process, lower cost of running the business — not because standards slip, but because the workforce is already keeping itself honest.

Private Equity Discovers the Same Thing

It is one thing to see this pattern in family businesses and founder-led companies that have practised it for a century. It is another to see a private equity firm — an industry not historically associated with generosity toward the workforce — arrive at the identical conclusion through hard data.

I've long admired Pete Stavros, Co-Head of Global Private Equity at KKR, for founding Ownership Works, a nonprofit dedicated to broadening equity ownership among employees and equipping them with the tools, data and transparency needed to understand and drive business success.

"Sharing stock ownership with workers and building 'ownership cultures' has proven time and again to be a win-win initiative," Stavros has said. "Ownership cultures work. Happier, more engaged employees lead to stronger businesses with more cohesive cultures and better returns."

KKR now has more than fifty portfolio companies applying the Ownership Works model. The early results are striking. KKR has reported roughly 4x returns in companies that adopted the model, compared with roughly 2.5x for its typical investments. Equity ownership is not a zero-sum game. Private equity earned its reputation in the 1980s through leverage and in the 1990s through roll-ups and conglomeration. Today, one of the most overlooked sources of value creation may simply be giving the people doing the work a meaningful stake in the value they create.

The Investor's Takeaway

For investors, the question is not simply whether executives own shares. That information is easy to find and already widely studied.

The more revealing questions sit further down the organisation. Do store managers participate in store performance? Do branch leaders understand the capital employed in their operation? Do frontline employees share in the wealth they help create? Is ownership broad or confined to the executive suite? Can employees see how their decisions affect customers, costs and cash? Are they trusted with enough authority to make those decisions matter? And when management says it wants people to act like owners, has it given them any reason to do so?

The answers may help explain why some companies retain exceptional people, control costs without bureaucracy, serve customers with unusual care and continue improving long after a charismatic founder has left.

Once again, none of this fits neatly into a discounted cash flow model. Employee ownership can create dilution. Profit sharing appears as an expense. Decentralised authority can look untidy. Paying an employee an unexpectedly large bonus may even trouble investors focused on next quarter's margin. But the best owners understand the trade. They are willing to divide the value more broadly when doing so enlarges the value available to divide. They know the difference between giving wealth away and sharing wealth with the people who helped create it.

Most companies already have plenty of employees. The exceptional ones build something more powerful.

A company of owners, not waiters.

* Visit the Blog Archive *

Learn more with us on Twitter: @mastersinvest

TERMS OF USE: DISCLAIMER