Warren Buffett doesn't have a computer on his desk. He buys stocks for the long run and he doesn't let short term stock prices impact his investing decisions. He advises investors "Don't watch the market closely" highlighting that when investors are "trying to buy and sell stocks, and worry when they go down a little bit - and think they should maybe sell them when they go up - they're not going to have very good results".

While it's important to keep abreast of developments at a company, it's important not to let a company's short term stock price move unduly influence investment decision-making. In many cases, short term stock moves are purely random phenomena.

"Some investors attach great importance to the daily or even hourly ups and downs, while others, like the undersigned, pay them no heed except when they present us with mouth-watering opportunity to do something." Frank Martin

As humans have evolved to feel losses significantly more than gains an investor who experiences a stock price decline maybe liable to make sub-optimal investment decisions.

“When directly compared or weighted against each other, losses look larger than gains. This asymmetry between the power of positive and negative expectations or experiences has an evolutionary history. Organisms that treat threats as more urgent than opportunities have a better chance to survive and reproduce.” Daniel Kahneman

“When an investor focuses on short-term increments, he or she is observing the variability of the portfolio, not the returns – in short, being “fooled by randomness”. Our emotions are not designed to understand this key point, but as investors, we need to come to grip with our emotional liabilities.” Barton Biggs

Nicholas Taleb, in his profound book, 'Fooled by Randomness', talks about the difference between noise and meaning. He uses the example of the happily retired dentist who builds himself a nice trading desk in his attic, aiming to spend every business day watching the market while sipping decaffeinated coffee. He watches his inventory of stocks via a spreadsheet with live price updates.

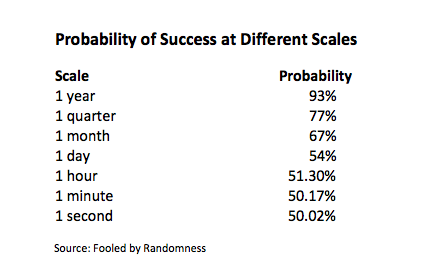

Taleb notes ..

"A 15% return with a 10% volatility (or uncertainty) per annum translates into a 93% probability of success in any given year. But seen at a narrow time scale, this translates into a mere 50.02% probability of success over any given second as shown in the table. Over the very narrow time increment, the observation will reveal close to nothing. Yet the dentist's heart will not tell him that. Being emotional, he feels a pang with every loss, as it shows in red on his screen. He feels some pleasure when the performance is positive, but not in equivalent amount as the pain when the performance is negative"

"Viewing it from another angle, if we take the ratio of noise to what we call non-noise (ie left column/right column), which we have the privilege of examining quantitatively, then we have the following. Over one month, we observe roughly 2.32 parts noise for every one part performance. Over one hour, 30 parts noise for every one part performance, and over a second 1,796 parts noise for every one part performance."

"Over a short time increment, one observes the variability of the portfolio, not the returns."

Allan Mecham of Arlington Value Capital [AVM] addressed the issue in his 2011 annual letter where he cited the historical odds of their fund outperforming the S&P500 in any given month over the preceding five years ...

"The data confirmed our suspicions: AVM performed 55% of the time - nearly a coin flip. This offers an interesting takeaway when combined with investors' inert psychology; had we reported monthly results, investors would have had the bizarre experience of disliking their exposure to top-notch gains (AVM's five year annualised return of 18.7% net of fees, versus -0.4% for the S&P500 would rank second out of 6,000 US equity funds tracked by Morningstar."

Many of the Investment Masters recognize the adverse psychological effects constant monitoring of a stock portfolio can have on investment returns.

“Almost all investors experience more pain and anguish from losses than they do pleasure from gains. The agony is greater than the ecstasy. I don’t know why this is true, but it is. Maybe it’s because the investment business breeds insecurity. But to the extent that the investor is focused on daily or even minute-by-minute performance of his or her portfolio, the time of pain is inadvertently increased and the time of pleasure reduced. The problem is that the investment pain leads to anxiety, which in turn can cause investors to make bad decisions. In other words continual performance monitoring is not good for your mental health or for your portfolio’s well-being, even though contemporary portfolio management systems and their suppliers, strenuously promote it.” Barton Biggs

“Well-worn studies confirm the financial utility of long-term viewpoints; however, behavioural psychologists augment the case by showing investors dislike losses two to three times more than they like gains. If short-term gains/losses carry 50/50 odds, then the disdain for losses implies that infrequent monitoring and long-term horizons aide both mental health and financial wealth. In short, Winston Churchill's quip on revenge may aptly apply to myopic investment habits: "Nothing costs more and yields less." Allan Mecham

"To be sure, the future is very abstract and provides little in the form of near-term emotional rewards. I've spent 40 years surrounded by people who watch the prices of the stocks they own as they fluctuate on a daily, or heaven forbid, hourly basis. Speeding through time on an emotional roller-coaster that ends where it starts is like envy: nothing good comes from the expenditure of enormous energy." Frank Martin

“Dick Thaler’s got a phrase, instead of watching CNBC, you should be watching ESPN. The idea being that tracking how you’re doing every day is going to cause tremendous unhappiness and it’s going to lead to more biases. Actually, we worked with one of our academic advisors, Professor Joey Engelberg who’s a UCSD and he’s done research that when the market goes down, there’s more admittances for heart attacks at the hospitals around the country.” Dr Raife Giovinazzo

“I try not to actually log in to the account unless I know I want to do something. I don’t want the daily blow-by-blow on prices. It’s bad for the investing psyche; it makes you impatient and lose perspective.” Chris Mayer

“When people can check their returns 30 times a minute on the internet, time horizons shrink, investors are impatient and sell at any sign of underperformance, so they fail to participate in periods of overperformance.” Joel Greenblatt

“The frequency with which an investor checks his investments plays a significant part in his or her level of risk aversion. As stocks go down on nearly as many days as they go up according to De Bondt and Thaler, stocks can be highly unattractive if they are observed on a daily basis. Other behavioralists have estimated that if an investor’s time horizon was 20 years, the equity premium would fall to 1.5% from 6% as there is very little chance an investor would experience a loss after so many years, and stocks would be a much more appealing investment.” Christopher Browne

To counter this psychological bias, some of the Investment Masters, like Buffett, try to keep away from quote screens during the day.

"If I have a Bloomberg on, I find I am looking what the market is doing. I am looking at every news story. I really like to be the one who is parsing the information, rather than having a lot of irrelevant information thrown at me." Lou Simpson

"I don't have my computer or Bloomberg monitor set up to show me the price of all my holdings on one screen; if I need to check the price of a stock, I do it individually so that I won't see the price of all my other stocks at the same time. I don't want to see these other prices unnecessarily and to subject myself to this barrage of calls to action. It's worth thinking a little more about the effect of all this gratuitous noise on my poor brain. Checking the stock price too frequently uses up my limited willpower since it requires me to expend unnecessary mental energy simply resisting these calls to action. Given that my mental energy is a scarce resource, I want to direct it in more constructive ways. We also know from behavioural finance research by Daniel Kahneman and Amos Tversky that investors feel the pain of loss twice as acutely as the pleasure of gain. So I need to protect my brain from the emotional storm that occurs when I see that my stocks or the market are down. If there's average volatility, the market is typically up in most years over a 20-year period. But if I check it frequently, there's a much higher probability that it will be down at that particular moment. (Nassim Taleb explains this in detail in his superb book Fooled by Randomness.) Why, then, put myself in a position where I may have a negative emotional reaction to this short-term drop, which sends all the wrong signals to my brain?" Guy Spier

“If you don’t like what’s happening to your shares, switch off the screen. The price of the shares you buy may vary for reasons which have nothing to do with the fundamentals of the business. So movements in share prices are not necessarily a guide to whether your investment is good or bad. If you have chosen shares in good companies or a fund at reasonable prices, and you find gyrations in their prices unsettling, then simply stop looking at the share price.” Terry Smith

“None of us have a Bloomberg terminal. We have an outsourced trader, in Vancouver. We don’t generally trade the same day we make decisions.” Yen Liow

"I try to be removed from the day-to-day: I don't have a ticker-tape machine in my office. I can read the papers. And there's an office nearby where I can go and watch it, but basically, I try to stay away from the emotions of the market. The market is a very emotional place that appeals to fear and greed. All these unpleasant characteristics that people have." Walter Schloss

By avoiding the impact of seeing short term losses an investor is more likely to be able to take a longer term perspective - a key edge in investing.

“Kahneman and Tversky were able to prove mathematically that individuals regret losses more than they welcome gains of the exact same size – two to two and one-half times more. It was a stunning revelation … If you don’t check your portfolio every day, you will be spared the angst of watching daily price gyrations; the longer you hold off, the less you will be confronted with volatility and therefore the more attractive your choices seem. Put differently, the two factors that contribute to an investor’s unwillingness to bear the risks of holding stocks are loss aversion and a frequent evaluation period. Using the medical word for short-sightedness, Thaler and Bernartzi coined the term myopic loss aversion to reflect a combination of loss aversion and the frequency with which an investment is measured… In my opinion, the single greatest obstacle that prevents investors from doing well in the stock market is myopic loss aversion.” Robert Hagstrom

“The more often people look at their portfolios, the less willing they will be to take on risk, because if you look more often, you will see more losses.” Richard Thaler

"You know, I think people’s investment would be more intelligent, you know, if stocks were quoted about once a year." Warren Buffett

With regards the trading dentist, Taleb concluded ..

"Now that you know that the high-frequency dentist has more exposure to both stress and positive pangs, and that these do not cancel out, consider that people in lab coats have examined some scary properties of this type of negative pangs on the neural system (the usual expected effect: high blood pressure; the less expected: chronic stress leads to memory loss, lessening of brain plasticity, and brain damage). To my knowledge there are no studies investigating the exact properties of trader's burnout, but a daily exposure to such high degrees of randomness without much control will have physiological effects on humans (nobody studied the effect of such exposure on the risk of cancer). What economists did not understand for a long time about positive and negative kicks is that both their biology and their intensity are different. Consider that they are mediated in different parts of the brain that the degree of rationality in decisions made subsequent to a gain is extremely different from the one after a loss."

Is it time to move that Bloomberg terminal?