Warren Buffett once said, half-joking, that the secret of life is weak competition. It's a strange thing for the world's most famous investor to admit — we're taught that competition is healthy, that rivalry sharpens products and disciplines prices. Buffett has spent sixty years looking for businesses that face as little competition as possible.

He's not alone. Charlie Munger put it more bluntly — he'd seen a single competitor be enough to ruin a business. Sam Zell argued there's no substitute for limited competition: you can be a genius, but if the field is crowded, genius won't save you. Peter Thiel turned it into a slogan: competition is for losers.

Chris Hohn makes the investor's case for why, stripped of the aphorisms. Moats aren't static, he argues — they're something you have to keep re-underwriting. "We used to love consumer staples, but they became richly priced and offered low returns. We used to like media content companies, but streaming severely weakened their moats. Disruption can happen — you've just got to stay alert to it." His fund's response is to spend almost all its time on barriers to entry precisely because most investors underestimate how quickly they erode.

The purest version of the ideal is the business with no competitors at all. Howard Stoeckel of Wawa liked to say the company didn't want to be McDonald's fighting Burger King — it wanted to be Cirque du Soleil, competing against no one, occupying a category so distinct that rivalry simply doesn't apply.

It's a beautiful position to be in. It's also rare, and it comes with a hidden risk. Chung Ju-yung, who built Hyundai, made the opposite case: a company without rivals eventually turns stagnant, the way state-run monopolies do — running alone in a marathon feels comfortable right up until the day it isn't. Markets move. Technology changes. A regulator shifts the rules, or a new entrant arrives with a better way of doing things. Comfort breeds blindness, and the business that has never had to look over its shoulder is often the last to notice the ground shifting beneath it.

And yet, set against Buffett’s crowd is an equally impressive group of builders who argue that competition made their businesses better, not worse. That is the paradox. The ideal business faces weak competition but behaves as though a formidable rival is always approaching.

Avoiding Competition

Some of the best operators didn't wait for weak competition — they engineered it, by staying invisible for as long as possible. Jeff Bezos has been explicit about this with AWS: "we got about two years of runway before competitors copy your idea," and in AWS's case, the head start ran to seven. Sam Walton said much the same about Walmart's early years, admitting the misconception that Walmart was a fly-by-night outfit "worked to our advantage," letting the company grow largely unnoticed until it was too far along to catch. Ingvar Kamprad built the same invisibility into IKEA's structure without ever naming it as strategy: stores went up out of town rather than in furniture retailers' traditional turf, tables were made by door manufacturers instead of furniture factories, and customers assembled the products themselves. None of it looked like competition to the incumbents — until IKEA was one of the most recognized furniture brands in the world.

The pattern shows up again and again in a company's choice of ground. Truett Cathy built Chick-fil-A inside shopping malls, a category fast food had ignored, and had it largely to himself for a decade. Enterprise Rent-A-Car avoided airports entirely, setting up next to Laundromats and strip malls while the majors fought over business travellers. Michael Dell built a direct-sales computer business that IBM and Compaq dismissed as "just a mail-order company" — until it wasn't. In each case, the competition wasn't absent by luck. It simply hadn't noticed yet.

Eventually, though, every successful business gets discovered. Then the question changes from how to avoid competition to how to use it.

Compete, Don't Retreat

In 1963, a Coca-Cola executive was asked what he thought of Pepsi. Robert Goizueta's answer became one of the more famous lines in American business: if Pepsi-Cola didn't exist, he said, he would try to invent it. It kept Coke — and Pepsi — lean, and on their toes. It's an odd thing to say about the company trying hardest to put you out of business. But wander through enough founders' letters and biographies, and you find the same instinct again and again: the best operators don't just tolerate their rivals. They study them, chase them, and sometimes seem almost grateful for them.

There's a cost to never facing a real rival, too. "Lack of competition is the equivalent of no peer review process," Michael Bloomberg argued — when a better competitor eventually shows up, an organization with no prior need to improve has usually grown too lazy to react in time. Charles Koch reached a similar conclusion from the builder's side of the equation: competition isn't something to survive, it's something to accelerate, and he's blunt about the tempting alternative — businesses that try to protect themselves through tariffs, permitting and subsidies end up trading away the very progress competition was supposed to produce.

The sharpest version of this idea belongs to A.P. Giannini, who built the Bank of America from a single branch into the largest bank in America. "If my opponents hadn't forced me time after time," he said, "there would have been no driving, sustained effort to top the field." Toward the end of his life, he went further, framing the debt as gratitude rather than grudging respect: "For whatever success I have attained, I give the bulk of the credit to my enemies. They stimulated me. They kept me going. I am thankful to them." It's the same instinct Ovid captured two thousand years earlier — a horse never runs so fast as when it has other horses to catch up to and outpace.

Your Competitor Is a Free Consultant

If the first instinct is to face competition rather than avoid it, the second is to actually learn from it. Nobody made the case better than Terry Leahy, who ran Tesco through two decades of brutal UK grocery competition:

"Years spent in the hurly-burly of retailing made me realise that competitors — and the act of competition itself — are great teachers. I don't like waiting for my competitors to come over the horizon. I prefer to seek them out. Nor am I interested in looking for their faults or spotting their weaknesses — that is not only easy to do, but a sign of complacency. I want to know about them so that I can learn from them. My strongest competitors are the best management consultants there are: I look at their operations, their products or simply visit their website to find out about their thinking, research and planning — for free."

Leahy named Aldi and Walmart as the two toughest competitors he faced at Tesco. When Walmart entered the UK, Tesco was genuinely worried — Walmart's buying power was formidable, and Tesco's non-food operation was still in its infancy. So Tesco studied them closely: "We crawled all over their business." What emerged was that Tesco's lean supply-chain expertise, built for fresh food, could offset the higher prices it paid manufacturers due to lower purchasing volumes. Tesco responded by increasing store size, launching new formats, broadening its product range, adding services and cutting prices. It also sourced more strategically, concentrating purchases with selected suppliers to recreate some of the scale advantages Walmart enjoyed through its enormous global buying power. The business didn't just survive the onslaught: Tesco grew market share and profits more in the five years after Walmart entered the UK than in the five years before. As Leahy put it, "Walmart drew the best out of us."

Henry Ford approached competition from the opposite direction. Whenever a new car appeared, he bought one, tore it down, and studied every improvement he could find. "Scattered about Dearborn," he said, "there is probably one of nearly every make of car on earth." Xerox, under David Kearns, benchmarked L.L. Bean's warehouse picking speed, American Hospital Supply's small-item logistics, and American Express's call resolution rate, pushing its own first-call resolution from near zero to 85 percent.

Sitting in the Car

Some of the best learning didn't come from formal benchmarking teams at all — it came from simply watching.

Tom Monaghan would sometimes drive to a competitor's pizza store and sit in the car for hours, estimating how much business they were doing and thinking through what might make them more successful — and, by extension, what might make Domino's more successful. He did the same outside his own stores. "The numbers weren't the important thing," he said. "What was important was the intellectual exercise." Over the course of building Domino's, he visited roughly three hundred pizzerias, purely to look for methods worth stealing.

Carl Sewell ran the reverse experiment on his chain of auto-dealerships, hiring mystery shoppers to buy cars from his own dealerships twice a year, so he could see his business the way a customer — or a competitor — would see it.

The Competitor You Don't Know You Have

The harder problem isn't the rival you can see. It's the one you can't.

Leahy borrowed an insight from the Cold War strategist Sir Michael Quinlan: expected threats are usually the ones everyone prepares for. The danger comes from what nobody thought to expect. Applied to business, Leahy's conclusion was that the more conventionally you define competition — the way analysts and industry experts define it — the less likely you are to spot the hidden competitor. "This is the greatest threat of all: the competition you don't know you have." Finding it requires ditching the analyst's frame and thinking like a consumer instead — someone with a need, a wish, a demand — and following instinct rather than convention.

Leahy learned this the hard way inside Tesco. The company built a non-food home-delivery service — washing machines, bikes — explicitly to beat Argos, a catalogue retailer. It eventually struck him that the assumption was entirely wrong. The real competitor wasn't Argos. It was Amazon, then mostly known for books, music and film, but clearly capable of expanding into new categories. Once he saw it, Tesco had to overhaul its processes, build new categories, and invest heavily in online capability and logistics to confront a competitor it hadn't originally been watching at all.

His broader observation was that the unexpected threat rarely comes from a competitor's deliberate move. It comes from a new piece of technology creating an entirely new sector that didn't exist when the original competitive map was drawn.

Cable had a version of the same blind spot, playing out on a much bigger stage. For decades the industry's competitive map was drawn against other cable operators and satellite. Netflix skipped that fight entirely — selling video straight to the consumer and delivering it over the very pipes cable had spent hundreds of billions of dollars building, without paying for the privilege. Within a few years it was consuming roughly a third of all North American internet traffic at peak hours, largely on content the cable networks had licensed to it themselves. Media veteran John Malone's verdict was blunt: the industry had funded its own demise. Cable had beaten every competitor it was watching for — it simply wasn't watching for this one.

Creative Destruction

Joseph Schumpeter gave this idea its theoretical name back in 1942, describing what he called creative destruction. His sharper point, echoed almost exactly by Leahy seventy years later, was about where the real danger comes from: "It is not... competition which counts, but competition from the new commodity, the new technology, the new source of supply [and distribution], the new type of organization... which strikes not at the margins of the profits and the outputs of the existing firms but at their foundations and their very lives."

Charles Koch built this thinking directly into how he runs his business. Creative destruction, he argues, is always with us — cars and trains replacing horses and buggies, smartphones and the internet replacing older forms of communication — and however good a business may be, "at some point, probably sooner than later, it will no longer be good enough." His stated aim is to "drive it faster than our best competitor" — treating the four sources of disruptive innovation Schumpeter identified (new products and services, new technologies, new sources of supply and distribution, new types of organization) as a menu to pursue rather than a threat to defend against.

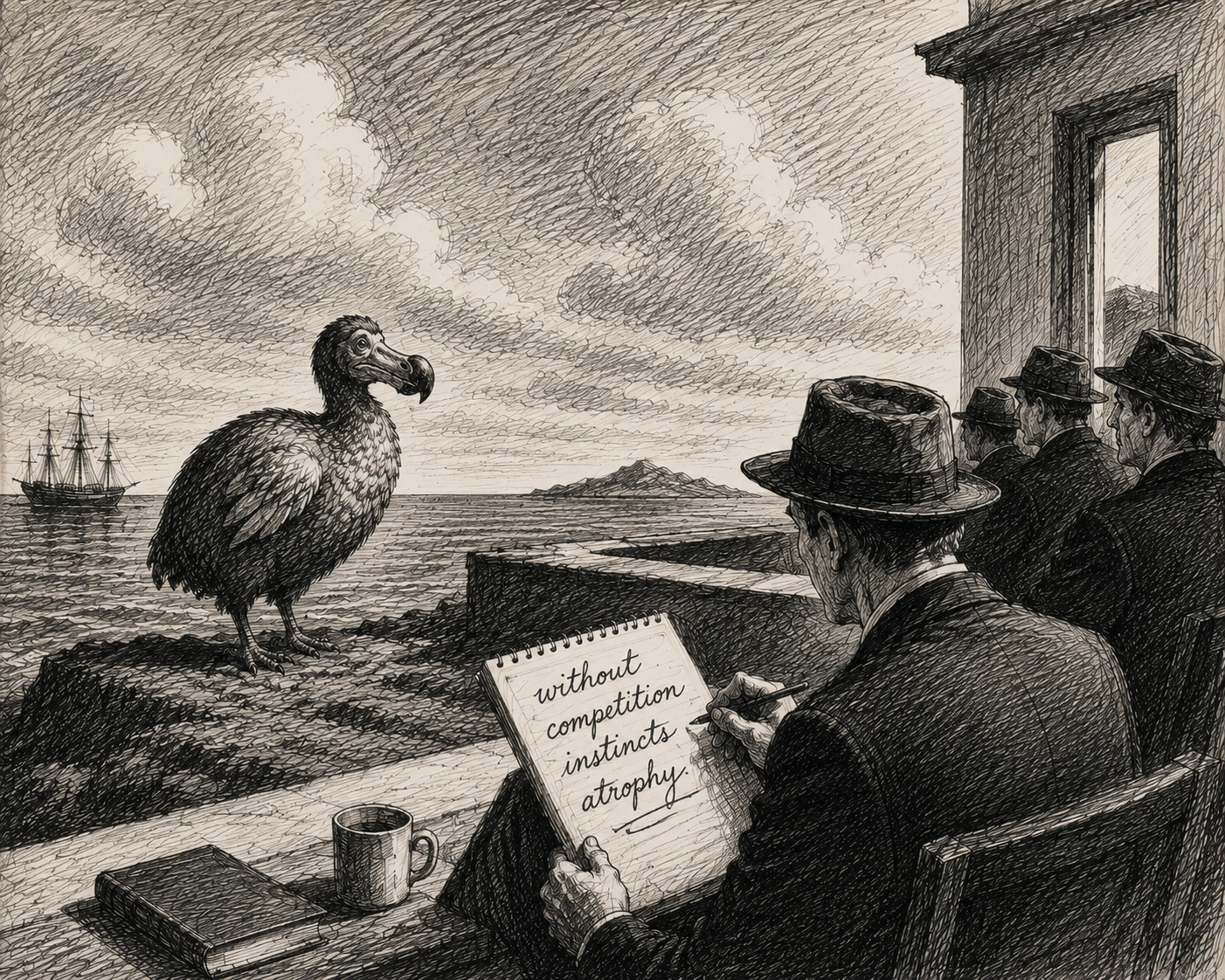

The Dodo Problem

There's a reason facing no real competitor at all is more dangerous than it looks.

Aoris Investment Management made the point using the dodo. The bird evolved on Mauritius, an island with no natural predators. With nothing to compete against, it lost the ability to fly and lost its fear instinct. It thrived for millions of years — right up until Dutch sailors arrived in 1598 with rats, pigs and monkeys that had been sharpened by real competition on the mainland. The dodo had no defences left, because it had never needed any.

Businesses that go unchallenged for long enough tend to lose the same instincts. Taxi companies are the more recent version of the same story. For decades, the incumbents faced limited competitive pressure and had correspondingly little incentive to invest in the product itself. Uber changed the category not by operating a better taxi fleet, but by introducing a technology layer the incumbents had never been forced to build: visibility, accountability and frictionless payment. It was Schumpeter’s warning made literal — a threat aimed not at the margins of the existing model, but at its foundations.

What Investors Should Look For

Most competitive-advantage analysis asks how far a business stands from its rivals: its scale, brand, switching costs, network effects or cost advantage. It is worth asking the opposite question too. How closely does management study its competitors? Does it know which competitor actually matters? And has it retained the instincts of a business that could still be challenged?

Weak competition is a wonderful economic advantage. But as Buffett put it just this month, "if you have a wonderful business, you are going to be subject to attacks. So it's not a question of whether it was wonderful yesterday — the question is, how long is it going to be wonderful?" Moats erode, technologies shift and competitors emerge from outside the categories analysts have learned to watch.

For investors, the tell is often in how management talks about its rivals. Is competition merely a risk-factor paragraph in the annual report, or does management understand how competitors operate, where they are improving and why customers might choose them instead? Has the definition of “competitor” been revisited recently, or is it frozen in the shape of the industry as it existed a decade ago?

The ideal business faces little competition but studies it relentlessly. It enjoys the economics of a monopoly without developing the instincts of one. Goizueta said he would invent Pepsi if it did not exist. Giannini simply thanked his enemies by name.

The secret may be weak competition. The trick is never believing it will stay that way.

Further Reading:

‘Iron Sharpens Iron: The Underappreciated Upside of Competition,’ Matthew Berry, Aoris Asset Management, March 2026.

* Visit the Blog Archive *

Learn more with us on Twitter: @mastersinvest

TERMS OF USE: DISCLAIMER