I recently read Creativity Inc, a book by Ed Catmull, who is co-founder of Pixar. Ed is a deep thinker, who after a two decade goal produced the first computer-animated feature film 'Toy Story'. Upon achieving this goal, and after recognising the missteps of other successful companies run by smart people, Ed devoted himself to the challenge of building a successful company with a sustainable creative culture that could outlast its founders.

Most of the books I read have been recommended by the Investment Masters, and Creativity Inc is no different. I can't recall which Investor recommended it, but I have seen it on quite a few recommended reading lists over time. I thoroughly enjoyed the book and it's no surprise it's highly recommended, the parallels in thinking between Ed Catmull and the Investment Masters are striking. Successful investing after all, requires creativity.

“We put great emphasis on a consistent investment process that demands enormous creativity, energetic sourcing, outside-the-box thinking, intellectual honesty, and vibrant debate.” Seth Klarman

“We think we try harder than most to be rational and creative. The combination of the two is important.” Nick Sleep

“It’s imperative to be creative because a stock currently is selling at a price that the average investor thinks is the right price, so you have to come to a decision that that price is wrong and that the stock deserves to sell at a higher price for some reason. That reasoning is creative thinking because other people aren’t thinking that way because if other people were thinking that way, the stock would be at a higher price. Every idea is a creative idea.” Ed Wachenheim

Creativity Inc, provides insights into how to enhance creativity and develop a creative culture. In many ways, Ed Catmull reminds me of Ray Dalio of the world's largest and arguably most profitable hedge fund, Bridgwater Associates. Both Ed and Ray have developed cultures that require high levels of transparency, seeking multiple viewpoints and consistently testing ideas. You'll notice many of the quotes below could have as easily been spoken by Ray Dalio as Ed Catmull. It's probably no surprise that both Ed and Ray cite Einstein as one of their idols.

"One of my favourite books is "Einstein's Mistakes" ... Provide people with as much exposure as possible to what’s going on around them. Allowing people direct access lets them form their own views and greatly enhances accuracy and the pursuit of truth." Ray Dalio

"Albert Einstein [was a boyhood hero]. I read every Einstein biography I could get my hands on as well as a little book he wrote on his theory of relativitiy. I loved how the concepts he developed forced people to change their approach to physics and matter, to view the universe from a different perspective. Wild-haired and iconic, Einstein dared to bend the implications of what we thought we knew. He solved the biggest puzzles of all, and in doing so, changed our understanding of reality." Ed Catmull

I've included some of the my favourite quotes below. Many of the sub-headings are topics from the Investment Masters Class tutorials [click on sub-headings to read tutorials].

TEAM DYNAMICS

"The leaders of my department understood that to create a fertile laboratory, they had to assemble different kinds of thinkers and then encourage their autonomy."

"My world view, forged in academia, that any hard problem should have many good minds simultaneously trying to solve it."

"I've made a policy of trying to hire people who are smarter than I am."

"When it comes to creative inspiration, job titles and hierarchy are meaningless."

"The responsibility for finding and fixing problems should be assigned to every employee, from the most senior to the lowliest person on the production line."

"What is more valuable, good ideas or good people? .. Ideas come from people .. To reiterate, it is the focus on people - their work habits, their talents, their lives - that is absolutely central to any creative venture."

"Find develop, and support good people, and they in turn will find, develop, and own good ideas."

QUESTIONS

"I've never stopped questioning."

"To foster a creative culture continually ask questions. Questions like : If we had done some things right to achieve success, how could we ensure that we understood what those were? Could we replicate them on our next project? Perhaps as important, was replication of success even the right thing to do?"

MISTAKES

"What makes Pixar special is that we acknowledge we will always have problems, many of them hidden from our view, that we work hard to uncover these problems, even if it means making ourselves uncomfortable"

"Mistakes are part of creativity."

"Mistakes aren't a necessary evil. They aren't evil at all. They are an inevitable consequence of doing something new (and, as such, should be seen as valuable; without them, we'd have no originality.)"

"Failure is a manifestation of learning and exploration. If you aren't experiencing failure, then you are making a far worse mistake: You are being driven by a desire to avoid it."

"In a fear-based culture, people will consciously or unconsciously avoid risk. They will seek instead to repeat something safe that's good enough in the past. Their work will be derivative, not innovative. But if you can foster a positive understanding of failure, the opposite will happen."

"Iterative trial and error - has long-recognized value in science. When scientists have a question, they construct hypothesis, test them, analyze them, and draw conclusions - and they they do it all over again. The reason behind this is simple. Experiments are fact-finding missions that, over time, inch scientists towards greater understanding. That means any outcome is a good outcome, because it yields new information."

"There are two parts to any failure: there is the event itself, with all its attendant disappointment, confusion and shame, and then there is our reaction to it. It is the second part we can contro.l"

"Failure gives us chances to grow, and we ignore those chances at our own peril."

"We get worried if a film is not a problem child right away. It makes us nervous."

"Discussing failure and all its ripple effects is not merely an academic exercise. We face it because by seeking better understanding, we remove barriers to full creative engagement."

"Companies, like individuals, do not become exceptional by believing they are exceptional but by understanding the ways in which they aren't exceptional. Post-mortems are one route into that understanding."

"The key to solving problems is finding ways to see what's working and what isn't, which sounds a lot simpler than it is."

HUMILITY

"The most compelling mechanisms [we follow] are those that deal with uncertainty, instability, lack of candor and the things we cannot see. I believe the best managers acknowledge and make room for what they do not know - not just because humility is a virtue but because until one adopts that mindset, the most striking breakthroughs cannot occur."

CONFIRMATION-COMMITMENT BIAS

"The more time you spend mapping out an approach, the more likely you are to get attached to it. The nonworking idea gets worn into your brain, like a rut in the mud. It can be difficult to get free of it and head in a different direction."

"There is nothing quite as effective, when it comes to shutting down alternative viewpoints, as being convinced you are right."

IDEAS

"Our job is to protect our [new ideas] from being judged too quickly. Our job is to protect the new.”

"At too many companies, the schedule (that is the need for product) drives the output, not the strength of the ideas at the front end."

TESTING IDEAS

"If someone disagrees with you, there is a reason. Our first job is to understand the reasoning behind their conclusions."

"The Braintrust [primary delivery system for straight talk] is one of the most important traditions at Pixar - It's premise is simple: Put passionate people in a room together, charge them with identifying and solving problems, and encourage them to be candid with one another."

"Most crucially, they [the Braintrust] never allowed themselves to be thwarted by the kinds of structural or perceived issues that can render meaningful communication in a group setting impossible."

"We are true believers in the power of bracing, candid feedback and the iterative process - reworking, reworking, and reworking again, until a flawed story finds its throughline or a hollow character finds its soul."

"We believe that ideas - and thus films - only become great when they are challenged and tested."

"The film itself - not the filmmaker - is under the microscope. This principle eludes most people, but it is critical: You are not your idea, and if you identify too closely with your ideas, you will take offence when they are challenged."

"People need to be wrong as fast as they can. In a battle, if you're faced with two hills, and you're unsure which one to attack. The right course of action is to hurry up and choose. If you find out it's the wrong hill, turn around and attack the other one."

"The key is to look at the viewpoints being offered, in any successful feedback group, as additive, not competitive."

"Seek out people who are willing to level with you, and when you find them, hold them close".

"There's a difference between criticism and constructive criticism. With the latter, you're constructing at the same time that your criticizing. You're building as you're breaking down, making new pieces to work with out of the stuff you've just ripped apart. That is an art form in itself."

CANDOR

"Telling the truth is difficult, but inside a creative company, it is the only way to ensure excellence."

"A fundamental Pixar belief: Unhindered communication was key, no matter what your position."

"Societal conditioning discourages telling the truth to those perceived to be in higher positions."

".. replace the word honesty with another word that has a similar meaning but fewer moral connotations - candor. No one thinks that being less than candid makes you a bad person (while no-one wants to be called dishonest.)"

"I truly believed that self-assessment and constructive criticism had to occur at all levels of a company, and I tried my best to walk the talk."

"A hallmark of a healthy creative culture is that its people feel free to share ideas, opinions, and criticisms. Lack of candor, if unchecked, ultimately leads to dysfunctional environment."

"Candor could not be more crucial to our creative process. Why? Because early on, all of our movies suck."

"Filmmakers must be ready to hear the truth; candor is only valuable if the person on the receiving end is open and willing, if necessary, to let go of things that don't work."

"Candor isn't cruel. It does not destory. On the contrary, any successful feedback system is built on empathy, on the idea that we are all in this together, that we understand your pain because we've experienced it ourselves."

CHANGE

"We are always changing, because change is a good thing."

"It's folly to think you can avoid change, no matter how much you want to. But also, to my mind, you shouldn't want to. There is no growth or success without change."

"I think the person who can't change his or her mind is dangerous."

"Everything is changing. All the time. And you can't stop it. And your attempts to stop it actually put you in a bad place. It causes pain., but we don't learn from it. Worse than that, resisting change robs you of your beginner's mind - your openness to the new."

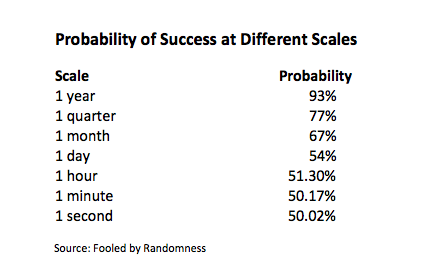

THE UNEXPECTED & RANDOMNESS

"Some people see random, unforeseen events as something to fear. I am not one of those people. To my mind, randomness is not just inevitable, it is part of the beauty of life. Acknowledging it and appreciating it helps us respond constructively when we are surprised."

"Randomness remains stubbornly difficult to understand. The problem is that our brains aren't wired to think about it. Instead, we are built to look for patterns in sights, sounds, interactions, and events in the world."

"How can we think clearly about unexpected events that are lurking out there that don't fit any of our existing models?"

"No matter how intensely we desire certainty, we should understand that whether because of our limits or randomness or future unknowable confluences of events, something will inevitably come, unbidden, through that door. Some of it will be uplifting and inspiring, and some of it will be disastrous."

"We must always leave the door open for the unexpected."

"The mechanisms that keep us safe from unknown threats have been hardwired into us since before our ancestors were fighting saber-toothed tigers with sticks. But when it comes to creativity, the unknown is not our enemy. If we make room for it instead of shunning it, the unknown can bring inspirations and originality."

"Randomness doesn't occur in a linear fashion."

GENIUS?

"The puzzle of trying to understand randomness: Real patterns are mixed in with random events, so it is extraordinarily difficult for us to differentiate between chance and skill."

"We must acknowledge random events that went our way, because acknowledging our good fortune - and not telling ourselves that everything we did was some stroke of genius - lets us make more realistic assessments and decisions."

WHAT YOU KNOW?

"When faced with complexity, it is reassuring to tell ourselves that we can uncover and understand every facet of every problem if we just try hard enough. But that's a fallacy. The better approach, I believe, is to accept that we can't understand every facet of a complex environment and to focus, instead, on techniques to deal with combining different viewpoints."

"Creativity demands that we travel paths that lead to who-knows-where. That requires us to step up to the boundary of what we know and what we don't know."

"While we know more about a past event than a future one - our understanding of the factors that shaped it is severely limited. Not only that, because we think we see what happened clearly - hindsight being 20-20 and all - we often aren't open to knowing more."

"Acknowledging what you can't see - getting comfortable that there are a large number of two-inch events occurring right now, out of sight, that will effect us for better or worse, in a myriad of ways - helps promote flexibility."

MENTAL MODELS

"Only about 40% of what we think we "see" comes in through our eyes. The rest is made up from memory or patterns that we recognise from past experience."

"We do have to function, so simultaneously, the brain fills in the details we miss. We fill in or make up a great deal more than we think we do. What I'm really talking about here are our mental models, which play a role in our perception of the world."

"All we need is a tiny bit of information to make huge leaps of inference based on our models - as I say, we fill it in."

"We have to learn, over and over again, that the perceptions and experiences of others are vastly different than ours."

"Successful leaders embrace the reality that their models may be wrong or incomplete."

"When humans see things that challenge our mental models, we tend not just to resist them but to ignore them. This has been scientifically proven. The concept of confirmation bias."

"If our mental models are mere approximations of reality, then, the conclusions we draw cannot help but be prone to error."

"Our mental models aren't reality. They are tools, like the models weather forecasters use to predict the weather. But as we know, all too well, sometimes the forecast says rain, and boom, the sun comes out. The tool is not reality. The key is knowing the difference."

"Our models of the world so distort what we perceive that they can make it hard to see what is right in front of us."

"I am constantly rethinking my own mental models for how to deal with uncertainty and change and how to enable people."

INNOVATION

"While experimentation is scary to many, I would argue we should be far more terrified of the opposite approach. Being too-risk averse causes many companies to stop innovating and to reject new ideas, which is the first step on a path to irrelevance."

RESEARCH TRIPS

"You'll never stumble upon the unexpected if you stick only to the familiar. In my experience when people go out on research trips, they always come back changed."

"Research trips challenge out pre-occupied notions and keep cliche's at bay. They fuel inspiration. They are, I believe, what keeps us creating rather than copying."

INTUITION & RIGHT BRAIN THINKING

"I've heard some people describe creativity as 'unexpected connections between unrelated concepts or ideas'. If that's at all true, you have to be in a certain mindset to make those connections."

"To have a "not know mind" is a goal of creative people. It means you are open to the new, just as children are."

"Paying attention to the present moment without letting your thoughts and ideas about the past and the future get in the way is essential. Why? Because it makes room for the views of others."

"Focusing on something can make it more difficult to see. The goal is to learn to suspend, if only temporarily, the habits and impulses that obscure your vision."

"While many activities use both L-mode [left brain] and R-mode [right brain], drawing required shutting the L-mode off. This amounted to learning to suppress that part of your brain that jumps to conclusions, seeing an image as only an image and not as an object... Artists [that] have learned to employ these ways of seeing [using techniques to engage only the right brain] does not mean they don't also see what we see. They do. They just see more because they've learned how to turn off their mind's tendency to jump to conclusions. They've added some observational skills to their toolboxes."

LEARNING

"I believe no creative company should ever stop evolving."

"Send a signal about how important it is for every one of us to keep learning new things. That, too, is a key part of remaining flexible: keeping our brains nimble by pushing ourselves to try things we haven't tried before."

When PIXAR embarks on a new film they are heading into the unknown. Similarly, an investor's results will be determined by the future. Both crafts demand creativity. It's no surprise Ed Catmull and Ray Dalio are both at the top of their field, and that they hold to similar ideals and virtues in their craft. Many of their life experiences have been similar but different - learning from their own mistakes and those of others, employing smart teams, changing the thinking paradigm and allowing innovative thoughts and creativity to be integral parts of their operations, being honest and open with yourself and others and above all to never stop learning - the day you think you know it all is the day you either need to stop, or start again from scratch.

We can use Ed Catmull as an example of how to go to 'infinity and beyond' .....